China’s Humanoid Robots Rush Toward Mass Production —

While Tesla Slows Down to Audit Suppliers. Here’s Why It Matters.

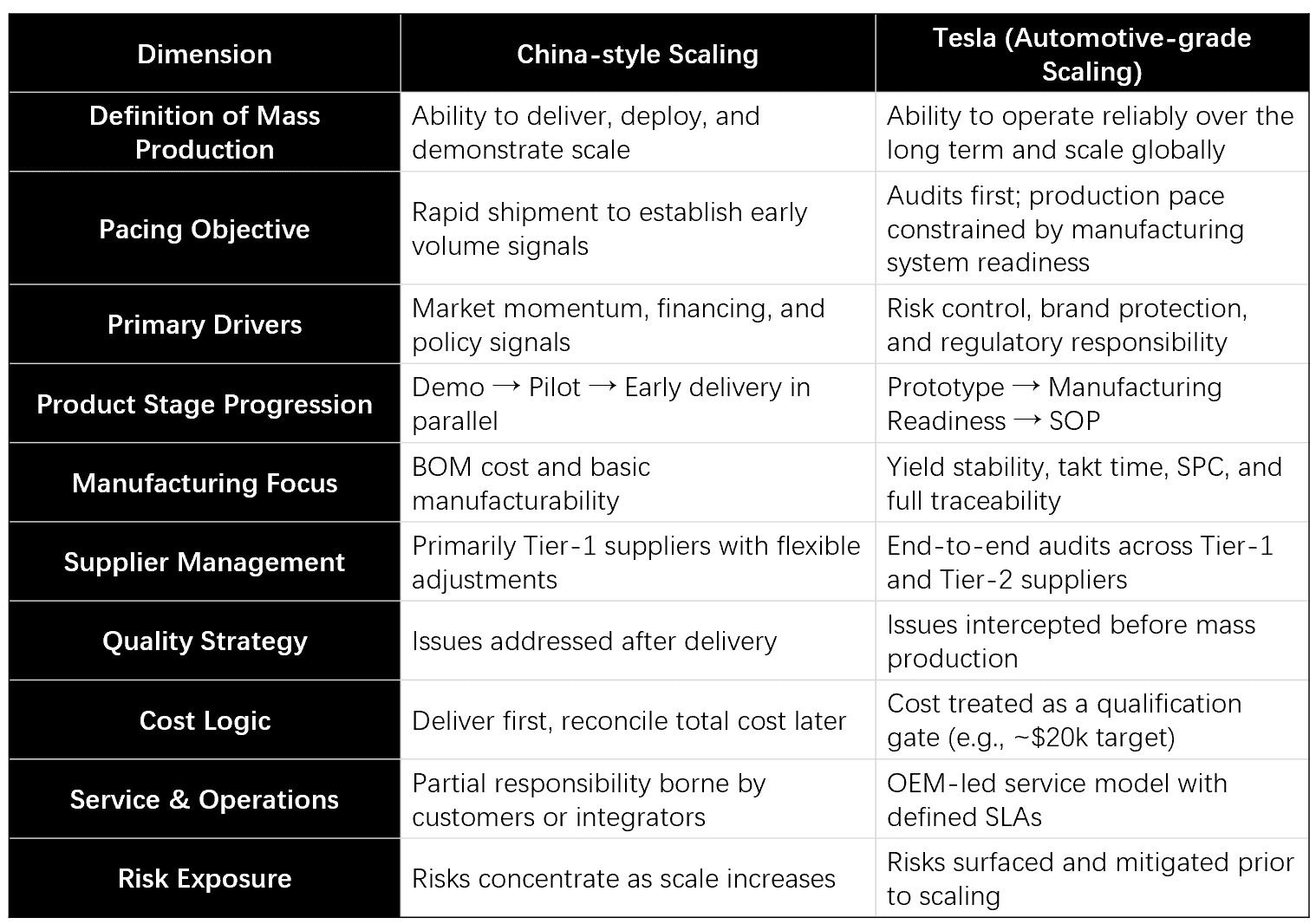

As humanoid robotics gains global momentum, a striking divergence is emerging. Across China, multiple humanoid robot companies are publicly accelerating toward mass production, announcing delivery targets, factory capacity plans, and early commercial deployments. In contrast, Tesla appears to be moving in the opposite direction: tightening supplier audits, reinforcing automotive-grade manufacturing standards, and deliberately slowing the transition from prototype to large-scale output for Optimus. At first glance, this contrast may look like a question of speed or confidence. In reality, it reflects fundamentally different risk models, incentive structures, and interpretations of what “mass production” truly means for complex humanoid systems.

Why China Is Pushing Volume — and Tesla Is Raising the Bar

Different Signals for Different Stakeholders

In China, early humanoid robot “mass production” announcements often function as market and policy signals. Delivery numbers, pilot deployments, and factory expansions serve to demonstrate momentum to investors, local governments, and ecosystem partners. In many cases, initial deployments occur in controlled, semi-public demonstration environments—industrial parks, logistics hubs, or government-backed pilot programs—where expectations are still flexible. Tesla’s incentives are fundamentally different. Once Optimus enters real-world workplaces at scale, any safety incident, prolonged downtime, or systemic failure becomes a brand, regulatory, and legal risk comparable to issues in the automotive industry. As a result, Tesla’s emphasis has shifted toward supplier auditing, manufacturing readiness, and long-term reliability, rather than headline delivery numbers.

Manufacturing Readiness vs. Manufacturing Appearance

The distinction Tesla is drawing is subtle but critical: manufacturing readiness is not the same as manufacturing appearance. A humanoid robot can be assembled, delivered, and even demonstrated at scale while still lacking the industrial maturity required for sustained deployment. Tesla’s supplier audits suggest a focus on deeper questions:

- Can yield remain above 95% over extended production runs?

- Can cycle time, takt time, and line balance remain stable across factories?

- Can cost targets—often cited near USD 20,000 per humanoid robot—be sustained without relying on hidden subsidies or deferred warranty costs?

- Can the supply chain absorb shocks, substitutions, and global replication?

These questions rarely surface in early-stage deployments, but they dominate outcomes once volumes grow.

What Happens When Complex Humanoids Scale Too Early

For humanoid robots, scale does not amplify success linearly—it amplifies failure nonlinearly. Before most key components and full systems accumulate long-term track records, rapid scaling tends to expose several predictable failure modes:

1. Reliability and Safety Risks Multiply

Joint modules, planetary roller screws, bearings, sensors, wiring harnesses, and thermal management systems all carry failure probabilities that compound with scale. In human-shared environments, even low-frequency failures can trigger regulatory scrutiny, insurance complications, and customer backlash.

2. Software Cannot Fully Mask Hardware Immaturity

OTA updates and AI policy improvements may improve behavior, but they cannot eliminate mechanical wear, tolerance drift, sensor degradation, or assembly inconsistency. Over time, software patches risk turning operations into configuration and version-management challenges rather than solving root causes.

3. Cost Curves Can Invert

Early unit economics often underestimate real costs. As return rates, field repairs, spare parts logistics, and on-site engineering hours accumulate, the true cost per deployed robot can exceed BOM estimates, turning “scale” into a loss multiplier rather than a margin lever.

4. Customer Operations Absorb Hidden Burdens

When robots require frequent human intervention, customers become de facto system integrators—managing resets, monitoring failures, and compensating for downtime. This erodes ROI, trust, and repeat adoption, even if headline deployment numbers look impressive.

The Overlooked Question: Who Operates 100,000 Humanoids?

One of the least discussed issues in humanoid robotics today is not manufacturing, but operations and support readiness.

If 100,000 humanoid robots are delivered into real-world environments, several questions become unavoidable:

- Who provides 24/7 on-time technical support?

- Who manages spare parts inventory, logistics, and replacement cycles?

- Who handles remote diagnostics, fleet monitoring, and software version control?

- Who assumes responsibility for uptime SLAs, safety compliance, and incident response?

In mature industrial robotics and automation markets, these questions are addressed through service networks, RaaS (Robot-as-a-Service) models, and long-term maintenance contracts. Without such infrastructure, large-scale deployment risks overwhelming both OEMs and customers.

Why Tesla’s Audit-First Strategy May Prove Rational

Tesla’s supplier audits—often described as strict or excessive—can be interpreted as a form of risk externalization and discipline enforcement. By embedding automotive-grade standards such as ISO 9001, IATF 16949, VDA 6.3, SPC, PPAP, and traceability requirements into supplier qualification, Tesla is effectively forcing the humanoid ecosystem to confront issues that many programs defer. Rather than betting on rapid deployment to surface problems later, Tesla appears to be pricing reliability, manufacturability, and serviceability into the system upfront.

A Likely Near-Term Outcome for the Industry

At the current stage of humanoid robotics development, a more probable industry trajectory may look like this:

- Selective scaling in controlled environments rather than broad, uncontrolled rollout

- Greater reliance on RaaS, managed fleets, and service-heavy deployment models

- Increasing convergence toward automotive-grade manufacturing and audit standards

- A widening gap between companies that can demonstrate demos and those that can sustain fleets

In this context, supplier audits are not a brake on innovation—they are a filter separating manufacturable systems from manufacturable illusions.

A Reality Check for the Humanoid Race

The humanoid race will not be decided by who delivers first—or even by who delivers most units in the short term. It will be decided by who can sustain reliability, cost control, supply chain resilience, and operational support over time.

Tesla’s audit-driven approach suggests a recognition that humanoid robots are no longer an AI experiment, but an industrial system with automotive-level consequences. For the broader industry, this may be an uncomfortable realization—but it is likely an inevitable one.

Two Scaling Philosophies in Contrast

Beneath the headlines about shipments and prototypes lies a deeper divergence: China and Tesla are not merely moving at different speeds—they are operating under fundamentally different definitions of what “mass production” means for humanoid robots.

Continue exploring Optimus coverage for updates on mass production timelines:

- Tesla Launches Final Audits of Potential Suppliers for Optimus (Mass Production I)

- Why Tesla's Audit Standards Redefine Humanoid Manufacturing (Mass Production II)

- China VS TESLA Two Paths to Humanoid Robot (Mass Production III)

Tesla’s Humanoid Robot Supply Chain coverage articles:

Why the Tesla Supply Chain for Optimus is Consolidating in Chinese Yangtze River Delta

Explains the geographic and industrial reasons behind the heavy concentration of Optimus suppliers in China's Yangtze River Delta region.

{kind=link}

Leave a comment