Brains vs. Brawn: CES 2026 and the Structural Split in Humanoid Robotics

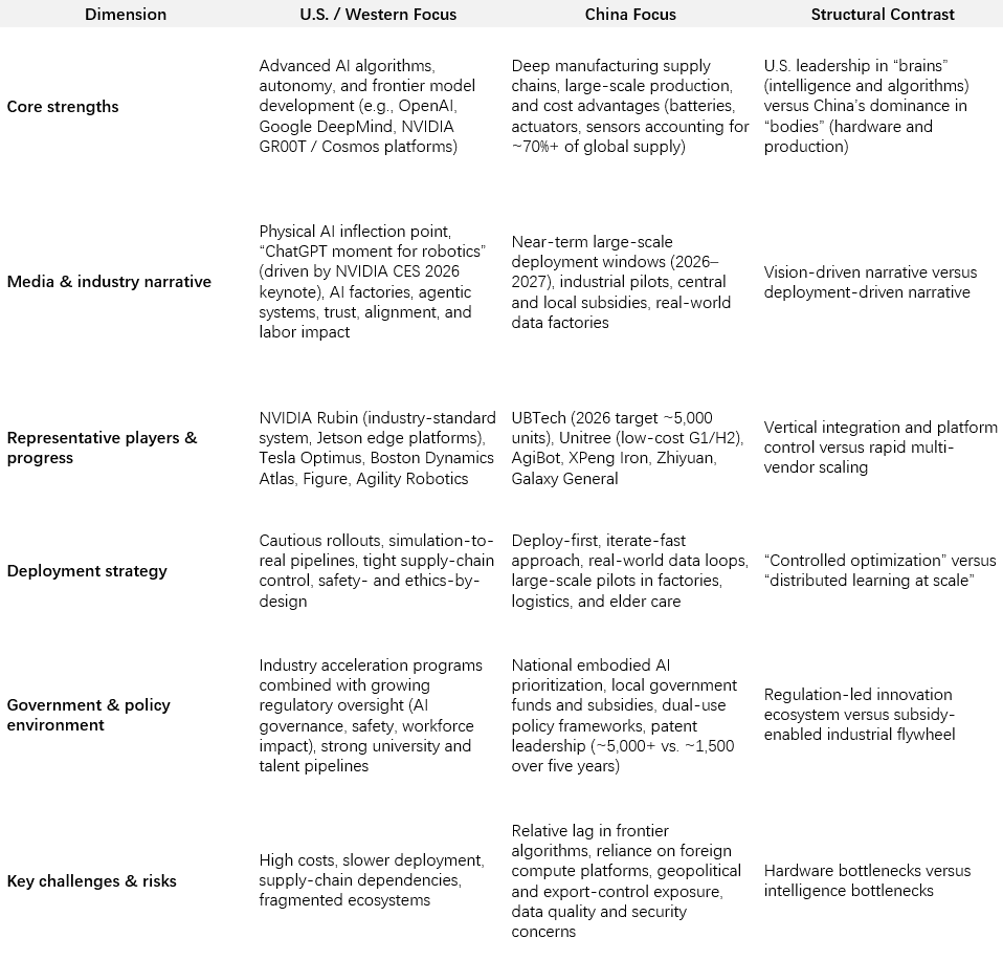

CES 2026 marked a clear inflection point for humanoid robotics, as a widening structural divide came into full view. On the keynote stage, Jensen Huang framed the moment as a “ChatGPT moment for physical AI,” unveiling NVIDIA’s Vera Rubin platform and positioning large-scale world models, simulation-to-real pipelines, and embodied intelligence as the core drivers of next-generation robots. The message was unmistakable: the United States continues to lead in the “brain” of humanoid systems—algorithms, compute platforms, and agentic reasoning.

Yet the CES show floor told a different story. Chinese manufacturers dominated physical presence, shipment volume, and price accessibility. Of the humanoid exhibitors at CES 2026, more than half were Chinese companies, with Unitree, AgiBot, and UBTech presenting production-ready platforms rather than concept prototypes.

The contrast was not cosmetic. It reflected a deeper asymmetry in how the U.S. and China are approaching humanoid robotics—and why neither trajectory, on its own, is likely to deliver scalable, economically viable systems.

Deployment Scale vs. Cognitive Sophistication

Shipment data from 2025 highlights the imbalance. Global humanoid robot shipments are estimated at approximately 13,000 units, with Chinese firms accounting for the majority. AgiBot alone is estimated to have shipped over 5,000 units, while Unitree and UBTech together contributed several thousand more. In contrast, U.S.-based programs—including Tesla Optimus, Figure, and Agility—remain largely in pilot-scale deployments, typically in the low hundreds.

This gap is not simply a matter of maturity. It reflects fundamentally different operating assumptions:

- U.S. players prioritize high-level autonomy, safety constraints, simulation-first training, and vertical integration.

- Chinese manufacturers emphasize rapid iteration, cost compression, and real-world deployment at scale, often supported by subsidies and integrated supply chains.

As a result, Chinese humanoids are already being deployed across factories, logistics centers, education, and research environments, generating continuous real-world data loops. U.S. systems, while often more sophisticated in perception and reasoning, remain constrained by cost and limited physical rollout.

Patents, Supply Chains, and Cost Curves

The structural divergence is reinforced by intellectual property and manufacturing control. Over the past five years, China has filed approximately 5,600–5,700 humanoid-related robotics patents, nearly four times the U.S. total. While patent volume does not equate to technical superiority, it reflects aggressive system-level experimentation—particularly in actuators, mechanical design, and integration.

More consequential is supply-chain dominance. Investment bank and industry estimates suggest China controls around 70% of the global humanoid robot component supply chain, spanning batteries, motors, reducers, sensors, and structural components. This concentration translates directly into cost advantages.

Industry estimates place the bill of materials for a Chinese-produced humanoid robot at roughly $40,000–50,000, compared with $120,000+ for systems built without access to Chinese supply chains. This cost differential explains why sub-$10,000 entry-level humanoids are already reaching universities and labs in China—something still largely unattainable for Western vendors.

All figures are best-available estimates based on public filings, analyst reports, and CES disclosures.

Why Neither Model Scales Alone

Despite the apparent imbalance, the data points to an uncomfortable conclusion: neither side’s approach is sufficient in isolation.

U.S. leadership in world models, embodied AI, and simulation-to-real learning defines how humanoids will eventually reason, adapt, and operate safely. But without affordable, mass-produced hardware, these advances remain confined to demonstrations and controlled pilots.

Conversely, China’s ability to deploy thousands of humanoids at low cost creates unparalleled data generation and iteration speed. Yet many of these systems still depend on Western compute platforms—particularly NVIDIA’s Jetson and Rubin-class processors—and lag in advanced autonomy and generalization.

The interdependence is already visible. Chinese humanoids frequently rely on U.S.-designed AI stacks, while Western models increasingly depend on Chinese manufacturing ecosystems to achieve viable cost curves.

Barriers to Convergence

This structural complementarity does not imply easy cooperation. Export controls, national security concerns, IP protection, and diverging regulatory philosophies are actively pushing the ecosystem toward fragmentation. The risk is the emergence of two parallel humanoid technology stacks—duplicating effort, inflating costs, and slowing progress.

From an industry perspective, fragmentation would be economically inefficient. From a technological standpoint, it would delay the feedback loop required to close the gap between cognition and embodiment.

A Structural, Not Ideological, Inflection Point

CES 2026 did not crown a winner in humanoid robotics. Instead, it clarified the underlying economics of the race. Intelligence without scale remains expensive. Scale without intelligence plateaus quickly.

For investors, engineers, and policymakers, the implication is pragmatic rather than ideological: the path to viable humanoid robotics runs through the integration of advanced AI systems with cost-efficient, high-volume manufacturing—wherever those capabilities reside. The question now is not which country leads, but whether the global ecosystem can reconcile innovation with deployment before fragmentation hardens into long-term inefficiency.

What this means for…

For robotics companies, the CES 2026 divide signals that success will hinge less on national origin and more on ecosystem positioning. Firms that combine advanced autonomy with access to scalable, cost-efficient manufacturing will move fastest from pilots to revenue.

For investors, shipment volume alone is no longer a proxy for defensibility. The critical question is whether a company sits inside a closed learning loop—where deployed hardware continuously improves embodied intelligence through real-world data.

For engineers and system architects, the challenge is integration rather than invention: standardizing interfaces between AI stacks, actuators, and edge compute will matter more than incremental algorithmic gains.

For policymakers, the risk is fragmentation. Parallel humanoid ecosystems would inflate costs, slow iteration, and delay economic impact. The competitive advantage will belong to those who enable controlled interoperability without compromising security or trust.

Related coverage from RobotToday:

- CES 2026 Robotics: From Physical AI to Real Deployment

Why humanoid development paths diverged sharply in readiness and execution - From iREX 2025 to CES 2026, Two Consecutive Stress Tests for the Global Robotics Industry

Why consecutive flagship events exposed structural pressure across the industry - CES 2026 Exposes a Structural Divide in Humanoid Robotics

The overarching framework connecting Physical AI concepts with real deployment

{kind=link}

Leave a comment