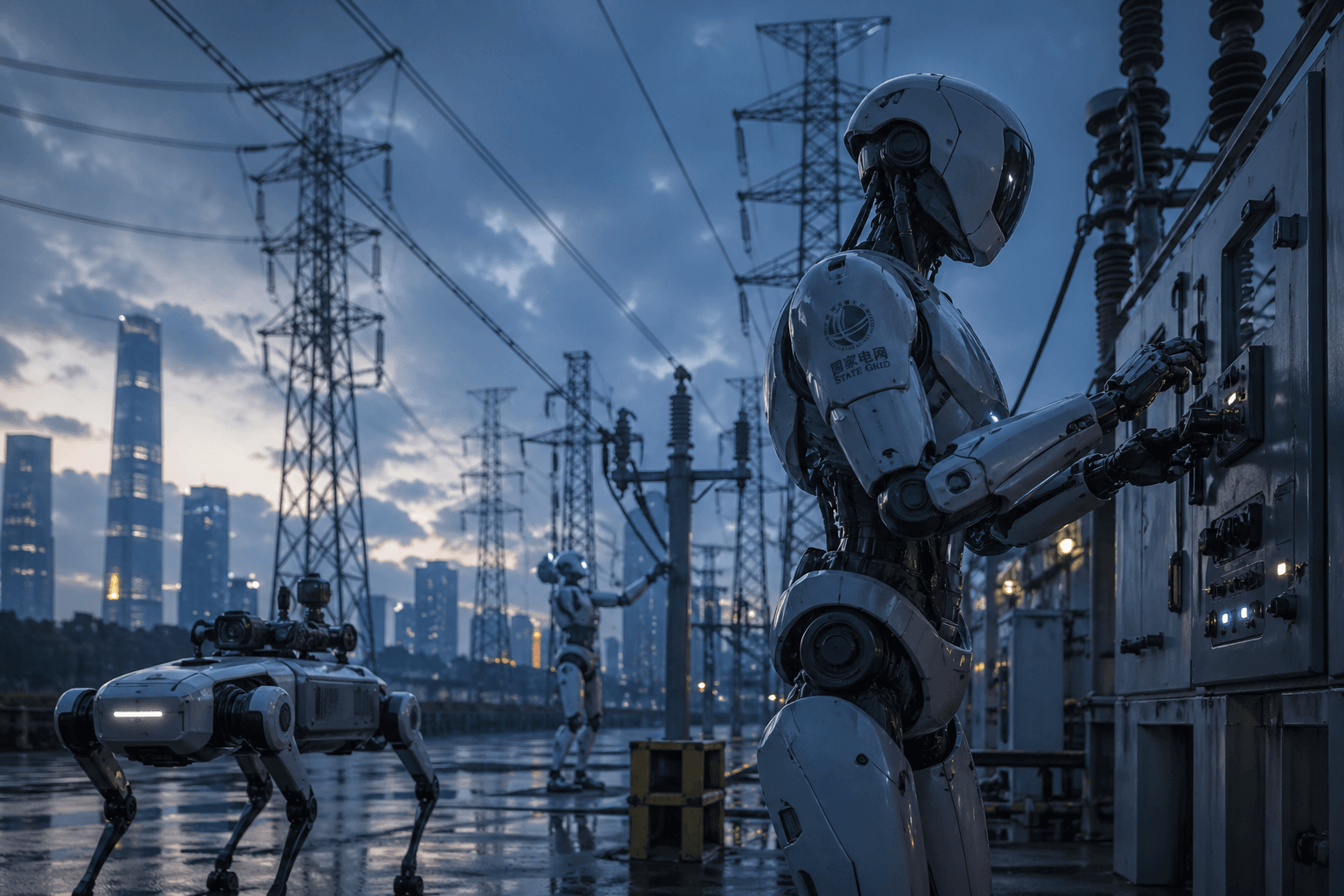

State Grid Corporation of China (SGCC) — the world’s third-largest company by revenue and operator of 80% of China’s national electricity grid — has quietly issued an internal plan to procure 8,500 robots at a total programme cost of approximately $938 million. If executed as planned, it will be the largest single embodied intelligence procurement ever recorded.

The plan, titled the 2026 Embodied Intelligence Development Plan, was circulated internally on April 22 and first reported exclusively by Jiemian News. SGCC has not published the document publicly, and no formal tender has been issued yet — but the scale and credibility of the buyer has already sent shockwaves through China’s robotics industry.

$938M Total plan value (hardware + R&D) | 8,500 Robots across three categories | $546B SGCC annual revenue (2023) | #3 Fortune Global 500 rank |

Who Is State Grid, and Why Does This Matter?

Before unpacking the robots, it helps to understand the buyer. SGCC is not a typical corporate customer.

Founded in 2002 as a state-owned enterprise under China’s electricity sector reforms, SGCC reported revenues of $546 billion in 2023 — placing it behind only Walmart and Amazon on the Fortune Global 500. It serves 1.1 billion customers, employs 1.3 million people, and has total assets of $781 billion. Its 2025 grid investment budget alone exceeds $89.6 billion.

SGCC is also a genuine technology pioneer. It has completed 38 Ultra-High Voltage transmission lines — a technology it leads globally — and operates the world’s largest fleet of pumped-hydro energy storage facilities. This is not an organisation that dabbles. When SGCC commits to a technology direction, it typically defines the trajectory for China’s entire energy infrastructure sector.

That context makes its pivot to embodied robotics significant well beyond the headline procurement figure.

What Is Being Bought

The plan allocates approximately $800 million to hardware across three robot categories, with a further $138 million for research, development, and talent:

PROCUREMENT BREAKDOWN BY CATEGORY

| Robot category | Units | Budget | Est. unit cost | Deployment |

| Quadruped inspection robots | 5,000 | $207M | $41,000 | Substations, mountainous terrain corridors |

| Humanoid live-line operation robots | 500 | $345M | $690,000 | Energised distribution networks, UHV projects |

| Dual-arm inspection robots | 3,000 | $248M | $83,000 | Substation equipment ops, fault response |

| Total hardware | 8,500 | $800M | — |

The total hardware investment of approximately $800 million represents 8.75% of SGCC’s annual smart infrastructure budget of $11.0 billion — a focused commitment within a much larger modernisation programme.

Who Stands to Win

No contracts have been awarded. The major centralised tender is not expected until Q3 2026, with a supplementary round in Q4. But the industry is already reading the tea leaves.

Media analysis and industry sources point to five Chinese manufacturers as frontrunners:

ANTICIPATED KEY VENDORS — PRE-TENDER ESTIMATES

| Company | Robot type | Est. share |

| UBTECH Robotics | Humanoid — Walker series | ~$221M |

| Yunjishen Technology | Quadruped — Jueying series | ~$207M |

| Zhiyuan Robotics | General humanoid platform | ~$193M |

| Fourier Intelligence | Dual-arm systems | ~$138M |

| Unitree Robotics | Quadruped and humanoid | $41M–$69M |

These estimates are projections from journalists and analysts and should be treated as directional only. The Q3 tender will determine actual winners, and SGCC is likely to run a competitive multi-vendor process.

One requirement that cuts across all categories: robots must integrate with SGCC’s proprietary “Guangming Power” large language model and support fully local data deployment. This effectively disqualifies vendors without credible AI software capabilities — raising the bar significantly above hardware specification alone.

The Bigger Picture: What This Signals for China’s Robot Market

SGCC’s order is best understood not as a single procurement event, but as the opening of a new industrial cycle.

The state enterprise cascade effect When a Chinese state-owned enterprise of SGCC’s stature formally commits to a technology category, it typically triggers parallel planning across the state enterprise ecosystem. China Southern Power Grid, provincial energy groups, and state-owned industrial operators are expected to follow. Total energy-sector robot investment could realistically exceed $1.4 billion within the next 24 months. |

The humanoid unit economics moment The 500-unit humanoid order at $690,000 per unit is not large by volume, but it matters enormously for the industry’s cost trajectory. Anchor orders from credible industrial buyers reduce financing risk for manufacturers, enabling the factory-scale investments needed to drive cost reduction. China’s solar and EV industries both followed this pattern — aggressive state-backed early deployment created the volume base that powered global competitiveness. |

AI software becomes the moat The Guangming Power LLM integration requirement signals a structural shift in how industrial robot contracts will be competed. Vendors that can offer a complete hardware-plus-AI stack — with on-premise deployment, safety certification, and integration into existing grid management systems — will have a durable advantage over pure hardware suppliers. |

Capital markets have already front-run the story Following the April 23 Jiemian News report, multiple robotics-adjacent equities gained more than 10% in a single session. Broader robotics exchange-traded funds in China saw elevated inflows, signalling institutional read-across to other state enterprise sectors. |

What to Watch

The coming months will clarify how much of the plan translates into signed contracts. Key milestones to track:

Q2 2026: Results from pilot deployments — particularly humanoid live-line operations — will either validate or complicate the Q3 tender scope

Q3 2026: Major centralised tender published on SGCC’s e-procurement platform. This is the definitive moment

Q3–Q4 2026: Listed companies announce material contracts via exchange disclosures

Full year 2026: Whether China Southern Power Grid or provincial energy operators issue similar plans

A Note on Information Quality

The 2026 Embodied Intelligence Development Plan remains an internal SGCC document. No full text has been made public. All specific budget allocations by category, and all vendor share estimates, originate from a single Jiemian News exclusive report and subsequent analyst commentary. Figures should be treated as credible but unverified until the official Q3 tender is published.

That said, SGCC’s scale, procurement track record, and the multi-outlet corroboration of the core figures give the story sufficient credibility to take seriously. This is not rumour — it is early-stage intelligence on a procurement that, if executed, will reshape China’s embodied robotics market for years to come.

Sources: Jiemian News (Apr 23, 2026); Cailian Press; 21st Century Business Herald; State Grid Corporation of China; Wikipedia; Brand Finance; MatrixBCG analysis. All CNY figures converted at 1 USD = 7.25 CNY (April 2026). Note: 1 亿 (yì) = 100 million CNY.

{kind=link}

Leave a comment