Why this comparison matters

During the 2021–2023 SPAC wave, robotics companies relied heavily on forward-looking revenue projections disclosed in Forms S-4 and S-4/A to justify merger valuations. These projections were legally framed as estimates, yet they became central to PIPE fundraising, investor expectations, and public-market pricing.

Once de-SPACed, however, those same companies entered a fundamentally different regime: audited financial reporting under Form 10-K, filed with the U.S. Securities and Exchange Commission. At that point, projections gave way to realized revenue. The gap between these two disclosure stages offers a rare, objective lens into how robotics commercialization actually unfolded.

Methodology

RobotToday reviewed revenue projections disclosed at the time of SPAC mergers (Forms S-4 / S-4A) and compared them with actual revenue reported in the first full fiscal-year Form 10-K following de-SPAC completion.

This analysis does not attempt to infer management intent or execution quality. Instead, it focuses on directional variance—how projected revenue timelines compared with audited outcomes once companies were subject to public-market disclosure discipline. All figures are rounded and sourced directly from SEC filings.

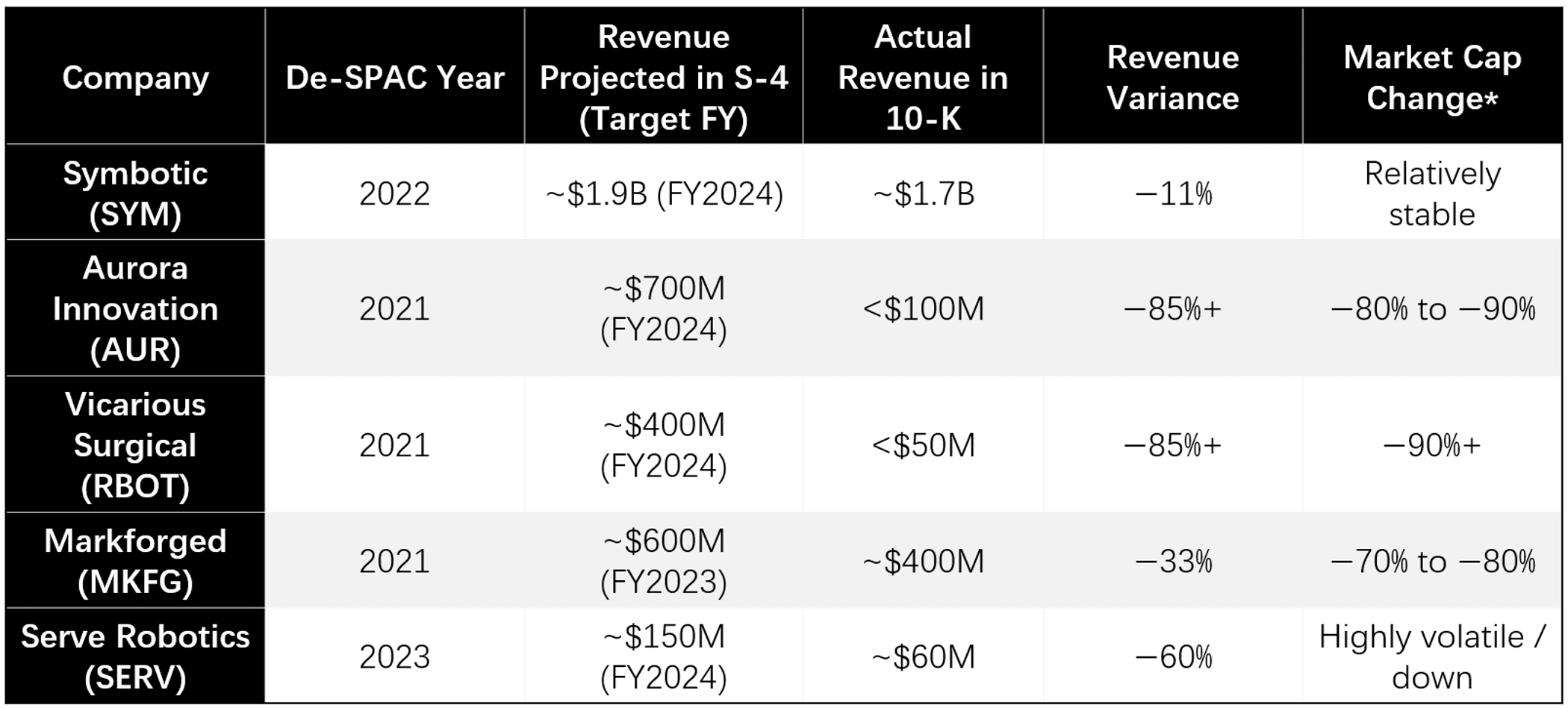

The numbers: projections versus reality; Revenue outcomes after de-SPAC

Market Cap Change reflects approximate directional change from post-de-SPAC peak valuation to recent public-market levels. Figures are indicative ranges only and influenced by broader equity-market conditions, interest-rate cycles, and sector sentiment. They are provided for contextual reference, not as a performance judgment.

What the revenue gap actually shows

The most important takeaway from this comparison is not that projections were “wrong,” but that revenue timing proved far more difficult than forecast.

Across multiple robotics verticals—warehouse automation, autonomous trucking, medical robotics, additive manufacturing, and last-mile delivery—the same pattern appears. Operating expenses generally scaled close to plan, while revenue realization lagged significantly. Customer validation cycles extended. Deployment density grew more slowly. Manufacturing ramps encountered supply-chain and integration constraints.

In other words, engineering and commercialization friction—not lack of demand—defined outcomes.

Why robotics was especially exposed

Robotics sits at the intersection of hardware, software, and operational deployment. Revenue recognition depends not only on product readiness, but on customer facilities, regulatory clearance, training, and long-term service integration. These constraints rarely compress on capital-market timelines.

SPAC projections, by design, compressed those timelines. Public-market reporting then decompressed them—immediately and visibly.

This dynamic explains why revenue gaps appear consistently larger in robotics than in asset-light software SPACs from the same period.

The broader implication for public-market robotics

Once companies transitioned from S-4 projections to 10-K reporting, valuation narratives shifted accordingly. Investor focus moved from long-term platform vision to near-term cash runway, backlog visibility, and unit economics.

Companies with contracted demand and narrow deployment focus retained credibility. Those reliant on broad, multi-use platform assumptions faced sustained pressure.

The public market did not invalidate robotics innovation. It re-anchored it to execution.

RobotToday takeaway

The S-4 versus 10-K revenue gap is not a footnote—it is one of the clearest empirical records of how robotics commercialization actually unfolded after the SPAC era.

For future robotics companies considering public markets, the lesson is straightforward: Projections are tolerated. Execution is priced.

Disclaimer This article is prepared by RobotToday for industry analysis purposes only and does not constitute investment advice. All financial data, risk factors, and business projections cited herein are sourced from publicly available filings, including Forms S-4/A, 8-K, 10-Q, and 10-K submitted to the U.S. Securities and Exchange Commission (SEC). Forward-looking statements referenced reflect management expectations at the time of disclosure and are subject to significant risks and uncertainties. RobotToday does not guarantee the accuracy or completeness of the information and assumes no liability for investment decisions made based on this content. Readers are encouraged to review the latest SEC filings for the most current information.

Related Analysis | Robotics After SPAC

- Beyond the SPAC Narrative: The Hard Reality of Robotics in the Public Market

Industry-wide performance patterns after robotics companies go public - S-4 Projections vs. 10-K Reality: Robotics After De-SPAC

How forecasted growth diverges from disclosed financials - Security Robotics After SPAC: Capital Reality and Supply-Chain Risk in the AlphaVest Merger

A case study of post-SPAC risk in a capital-intensive vertical

{kind=link}

Leave a comment