On June 19, 2026, Reuters filed a brief dispatch: Hyundai Motor Group would acquire SoftBank's remaining 9.65% stake in Boston Dynamics for $325 million.

The news itself was not a surprise. What merits closer reading is the five years of groundwork behind the transaction — and what it signals about the phase the robotics industry is now entering.

I. A History of Changing Hands

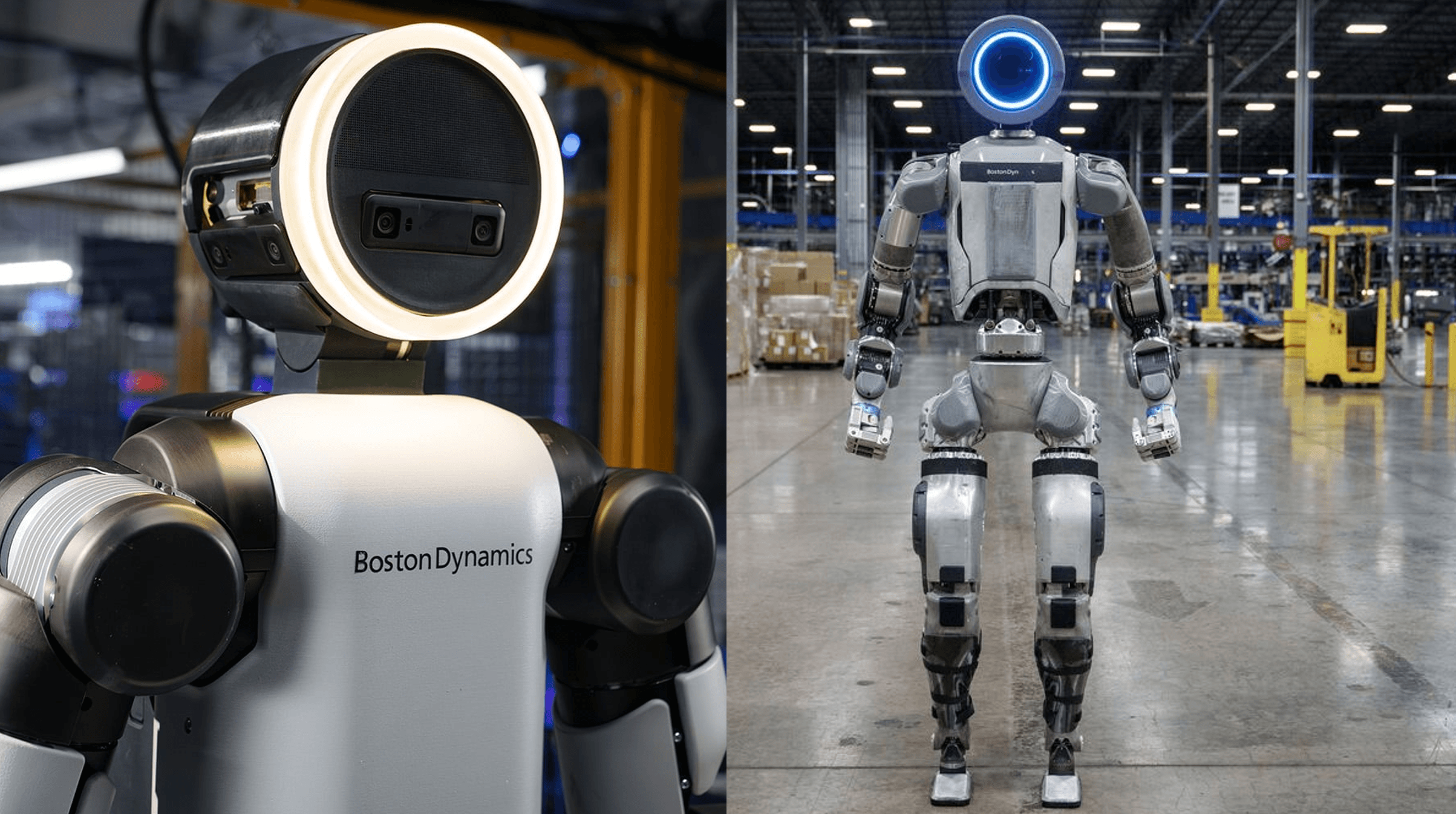

Boston Dynamics was founded in 1992 inside a Massachusetts Institute of Technology laboratory, sustained for two decades by grants from DARPA and similar institutions. Its robots could backflip and navigate broken terrain. Selling them was never quite the point.

In 2013, Google folded it into the Google X robotics division, hoping it might anchor the company's ambitions in automation. Within a few years, the mismatch between Boston Dynamics' research cadence and Google's commercial expectations became apparent, and the company was quietly put up for sale.

SoftBank acquired it in 2017 at a significant premium, slotting it into a broader robotics portfolio backed by the Vision Fund. The same problem persisted. One product — the quadruped Spot — reached commercial sales, but revenue remained modest against the scale of investment.

In June 2021, Hyundai Motor Group completed its acquisition of a controlling 80% interest, valuing the company at $1.1 billion, with SoftBank retaining the remaining 20%. Embedded in that agreement was a put option: if Boston Dynamics failed to complete a U.S. IPO within a specified window, SoftBank could require Hyundai to repurchase its remaining shares at a contractually agreed price.

The deadline was June 2026.

II. The Trigger: An Ending Written on Day One

The IPO did not happen. SoftBank notified Hyundai of its intention to exercise the put option, and Hyundai is expected to convene a board meeting on June 22 to formally approve the $325 million buyback.

SoftBank's exit follows a straightforward logic. The contractual mechanism was triggered. Beyond that, investment activity by Hyundai subsidiary Glovis last August implied a Boston Dynamics valuation of approximately $22 billion — roughly 24 times the $1.1 billion figure from the 2021 transaction. The put option price was anchored to that original valuation, which means SoftBank is effectively exiting at a steep discount to current implied market value. For an investment group increasingly concentrated on AI infrastructure and data centers, recovering capital from a minority position in an as-yet-uncommercial robotics company is the more pragmatic outcome.

The timing is deliberate on Hyundai's part as well. With Atlas scheduled to enter commercial production in 2026, clearing the ownership structure ahead of that milestone means Hyundai faces no minority shareholder constraints at the most consequential moment in Boston Dynamics' history.

III. Hyundai's Calculus: The Case for Vertical Integration

Hyundai's interest in Boston Dynamics was never purely financial.

Automotive manufacturing is among the world's most demanding supply chain environments — actuators, sensors, precision components, assembly tolerances. The capabilities required to build a competitive humanoid robot overlap substantially with what large-scale car production already demands. Hyundai's own factories are simultaneously the most natural customer for Boston Dynamics' products and their most valuable testing environment: material handling, assembly line support, quality inspection — each real-world task generating operational data that feeds back into model development and hardware iteration.

The publicly stated roadmap reflects this logic. Atlas is scheduled to begin scaled deployment at Hyundai's Metaplant facility in Georgia in 2028, initially handling parts sorting before expanding into assembly tasks, with a cumulative target of 30,000 units deployed across group subsidiaries by 2030.

The strategy is coherent. The execution risk is not small.

IV. The Friction

Hyundai has invested more than $2.2 billion in Boston Dynamics to date, against approximately $270 million in revenue. Losses continue to accumulate. At the production level, the gap between ambition and current reality is stark: supply chain data suggests the electric Atlas is being manufactured at a rate of roughly four units per month.

Between that figure and a 30,000-unit deployment target lies an engineering and manufacturing challenge that a cleaner ownership structure does not resolve.

The company has also seen significant management turbulence at an inopportune moment. Several senior executives, including the Chief Technology Officer, departed during the IPO preparation period, with some taking positions at competitors including Google. Concentrated leadership attrition ahead of a major capital markets event tends to register in investor perception as evidence of internal disagreement over commercial direction or governance.

External competitive pressure is intensifying. Tesla continues to advance Optimus on a manufacturing-at-scale thesis. Chinese manufacturers — Unitree, Zhiyuan, Fourier Intelligence among them — are compressing humanoid robot costs and moving toward volume production at price points well below Boston Dynamics' current range, while pursuing their own capital markets listings. Boston Dynamics' technical depth is real and its accumulated intellectual property is substantial. The distance between technical leadership and commercial leadership in this sector, however, remains genuinely difficult to measure.

V. The Larger Frame

Viewed narrowly, this is a routine equity repurchase triggered by a contractual mechanism. In a wider context, it marks something closer to an inflection point.

Scaling humanoid robots from laboratory demonstration to factory deployment requires more than engineering excellence: manufacturing capacity, verified use cases, supply chain integration, and patient capital operating under a unified decision-making structure. Full ownership concentrates all of those requirements under a single institutional mandate.

Analysts expect Boston Dynamics could pursue a Nasdaq listing as early as 2027 or 2028. When that process begins, the valuation Boston Dynamics commands will set a reference point for the entire robotics supply chain — precision reducers, force-control sensors, AI chips, battery systems. The question the company will need to answer for Wall Street is whether a production curve that currently reads four units a month can inflect sharply upward within a two-year window.

SoftBank's departure transfers that question entirely to Hyundai.

[1] Reuters — Primary news wire report (June 19, 2026)

Hyundai to buy SoftBank's remaining stake in Boston Dynamics for $325 mln, newspaper says

↳ Core transaction details: $325M consideration, 9.65% stake, June 22 board meeting, put option exercise.

[2] Business Recorder / Reuters (June 19, 2026)

Hyundai to buy SoftBank's remaining stake in Boston Dynamics for $325 mln

↳ Confirms group structure: Hyundai Motor, Kia, Hyundai Mobis, Hyundai Glovis, and Euisun Chung already hold >90%.

[3] Global Banking & Finance Review (June 19, 2026)

Hyundai to buy SoftBank's remaining stake in Boston Dynamics for $325 million

https://www.globalbankingandfinance.com/hyundai-buy-softbanks-remaining-stake-boston-dynamics-325/

↳ Valuation data: Hyundai Glovis investment (Aug 2025) implied ~30 trillion KRW (~$22B), a ~24x increase over the 2021 figure.

{kind=link}

Leave a comment