Global Industrial Robotics Report 2026 Edition

The industrial robotics market encompasses an extraordinarily diverse range of hardware architectures, payload classes, application domains, precision tiers, and drive technologies. A single-axis classification — 'industrial robot' versus 'collaborative robot' — no longer captures the nuance required for investment-grade analysis. This chapter introduces a Five-Dimensional Scientific Classification System that cross-cuts all product categories and enables precise market sizing, competitive benchmarking, and technology-roadmap assessment.

Data sources: IFR World Robotics 2025 (released September 2025, based on 2024 installation data); MarketsandMarkets Industrial Robotics Report 2024-2029; Grand View Research; Precedence Research; GlobalInfoResearch; company annual reports (FANUC, ABB, KUKA, Yaskawa, Universal Robots).

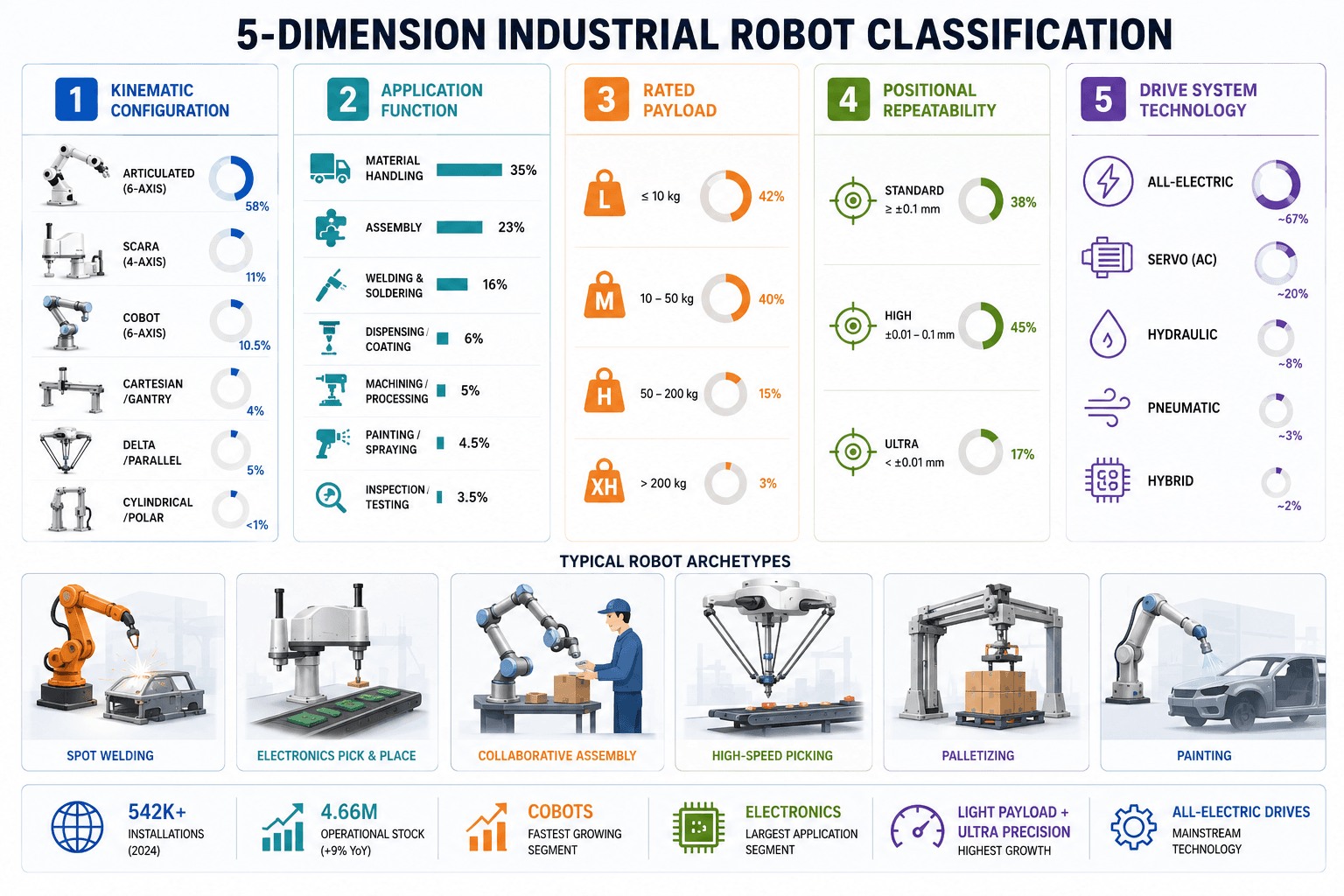

1 Dimension I — Kinematic Configuration

Kinematic configuration is the primary axis of differentiation. The IFR records six standard robot types; in 2024 global installations totaled 542,000 units — the fourth consecutive year above 500,000 — with a cumulative operational base of 4.664 million units (+9% YoY).

Robot Type | Structure | 2024 Installations | Market Share | Key Applications |

|---|---|---|---|---|

| Articulated (6-axis) | 6-axis rotary joints, reach 500-4,000 mm | >= 375,000 units | ~58% | Welding, painting, assembly, handling |

| SCARA (4-axis) | Selective compliance, horizontal reach | >= 61,000 units | ~11% | Electronics assembly, soldering, pick-and-place |

| Collaborative (Cobot) | Force-limiting, 6-axis, all-electric | ~57,000 units | ~10.5% | SME assembly, inspection, human-robot co-work |

| Cartesian / Gantry | Linear XYZ axes, high payload at large span | ~22,000 units | ~4% | CNC loading, palletizing, large-part assembly |

| Delta / Parallel | 3-arm, ultra-high speed >= 150 picks/min | ~27,000+ units | ~5% | Food packaging, pharma, electronics sorting |

| Cylindrical / Polar | Rotary + linear axis, niche legacy installs | < 5,000 units | < 1% | Spot welding, die casting (legacy) |

Sources: IFR World Robotics 2025; GMInsights Industrial Robotics Market 2025-2034; MarketsandMarkets 2024. Cobot share per IFR 2023 official data (10.5%); 2024 figure not yet separately disclosed.

Key Structural Insight

Articulated robots have held ~58% share for over a decade. Cobots are the fastest-growing sub-segment at a projected CAGR of 23.1% (2026-2033), driven by SME penetration and the Robotics-as-a-Service (RaaS) subscription model. Delta robots, while <5% of volume, command premium ASPs in pharmaceutical and high-speed food packaging verticals.

2 Dimension II — Application Function

IFR classifies applications into seven primary functions. In 2024, the electrical/electronics industry led installations at 129,000 units (+2% YoY), narrowly overtaking automotive at 126,000 units (-7% YoY). The food & beverage segment surged 42% YoY — the largest single-year growth rate across all verticals.

Application | Revenue Share | CAGR 2024-2032 | Lead Industry | Representative Robot |

|---|---|---|---|---|

| Material Handling | ~35% | 11.8% | Automotive, Logistics | Articulated, Cartesian |

| Assembly | ~22.7% | 13.2% | Electronics, Automotive | SCARA, Articulated |

| Welding & Soldering | ~15.5% | 10.4% | Automotive | Articulated 6-axis |

| Dispensing / Coating | ~6% | 9.8% | Electronics, EV Battery | Articulated, SCARA |

| Machining / Processing | ~5% | 9.1% | Metal, Aerospace | Heavy Articulated |

| Painting / Spraying | ~4.5% | 8.6% | Automotive | Hollow-wrist Articulated |

| Inspection & Testing | ~3.8% | 15.6% | Electronics, Pharma | Cobot, SCARA |

Sources: SNS Insider Industrial Robotics Market 2032; Fortune Business Insights Robotic Welding 2034; Market.us Industrial Robotics Market 2024. Shares are revenue-weighted estimates.

A structural shift is underway: automotive's share of global installations fell from ~40% historically to ~23% in 2024, while electronics eclipsed it. This mirrors the macro trend of electronics and EV battery manufacturing becoming the new capital-expenditure frontier for robotics investment.

3 Dimension III — Rated Payload

Payload capacity is a direct proxy for robot cost, energy consumption, and addressable industry. Four commercial tiers have emerged as the industry-standard segmentation.

Payload Tier | Range | Revenue Share | CAGR | Key Application |

|---|---|---|---|---|

| Light-Duty | < 16 kg | ~28% | 14.8% | Electronics assembly, cobot tasks |

| Medium-Duty | 16 - 60 kg | ~33% | 12.1% | General automotive, machining |

| Heavy-Duty | 61 - 225 kg | ~27% | 10.3% | Spot welding, body-in-white |

| Ultra-Heavy | > 225 kg | ~12% | 8.9% | Foundry, shipbuilding, aerospace |

Sources: Precedence Research Industrial Robotics Market 2034. Cobot sub-segmentation: <=5 kg = 45% of cobot market revenue (Grand View Research Collaborative Robots Market 2033).

The light-duty tier exhibits the highest CAGR, propelled by the cobot boom and miniaturization of semiconductor and consumer electronics assembly. Cobots with payload <=5 kg accounted for 45% of 2024 cobot revenue, validating the 'right-sizing' trend where over-engineered heavy arms are replaced by flexible light-duty cells.

4 Dimension IV — Repeatability Precision

Repeatability — the ability to return to a taught position under identical conditions — is the primary precision metric for industrial robots, and the specification cited in virtually all procurement decisions (ISO 9283).

Precision Tier | Repeatability | Typical Robot Type | Application Domain | Price Premium |

|---|---|---|---|---|

| Standard | +/- 0.1 - 0.5 mm | Heavy articulated, Cartesian | Welding, palletizing | Baseline |

| High Precision | +/- 0.02 - 0.1 mm | Mid-range articulated, SCARA | General assembly | +15% - 30% |

| Ultra-Precision | +/- 0.005 - 0.02 mm | Small SCARA, cobot, delta | Semiconductor, medical | +40% - 80% |

| Nano-Precision (emerging) | < +/- 0.005 mm | Specialized cleanroom robots | Wafer handling, optics | > +80% |

Note: Repeatability specs are manufacturer-stated under ISO 9283:1998 standard test conditions. Real-world performance may vary +/-20-30% due to thermal drift, load variability, and wear. Sources: ABB, FANUC, Yaskawa product datasheets.

The most significant market development in this dimension is the rapid commercialization of ultra-precision cobots for semiconductor backend processes. As chip packaging pitches shrink below 10 micrometers, dedicated robots achieving +/-5 micron repeatability command pricing of USD 80,000-250,000 per unit and grow at double the market average.

5 Dimension V — Drive System

The drive system determines energy efficiency, maintenance cycle, operating environment suitability, and total cost of ownership. Electric drives captured an estimated 53% of the robotics actuation market in 2024.

Drive Type | Market Share | Energy Efficiency | Maintenance Cycle | Typical Use Case |

|---|---|---|---|---|

| Electric (AC Servo) | ~53% | Very High | Low (5,000-10,000 h) | All articulated, SCARA, cobot |

| Pneumatic | ~28% | Low | Medium (2,000-4,000 h) | Pick-and-place, delta robots |

| Hydraulic | ~12% | Medium | High (1,000-2,500 h) | Heavy foundry, forging |

| Hybrid Electric-Hydraulic | ~5% | Medium-High | Medium | Large stamping, aerospace |

| Piezoelectric / Other | ~2% | Very High | Very Low | Nano-precision, cleanroom |

Sources: Market.us Robotics and Automation Actuators Market 2024; Grand View Research Servo Motor Market 2030. Electric drive share is a composite estimate from the robotics actuator market.

The servo motor market underpinning electric drives was valued at USD 13.52 billion in 2024, projected to reach USD 20.13 billion by 2030 at CAGR 6.9%. The precision gear reducer market was valued at USD 2.84 billion in 2024: harmonic reducers hold ~41% share, RV reducers ~37%. Japanese manufacturers Harmonic Drive Systems and Nabtesco historically controlled >70% combined global supply before Chinese competitors began eroding share from 2021 onward.

6 Five-Dimensional Matrix — Strategic Synthesis

The five dimensions interact to define product archetypes. The table below maps the three highest-volume commercial archetypes across all five dimensions simultaneously.

Dimension | Archetype A: Automotive Spot Welder | Archetype B: Electronics SCARA | Archetype C: Collaborative Cell |

|---|---|---|---|

| D1 Configuration | 6-axis articulated | 4-axis SCARA | 6-axis force-limited cobot |

| D2 Application | Spot welding | High-speed assembly | Flexible assembly + inspection |

| D3 Payload | 165 - 350 kg | 3 - 20 kg | 3 - 16 kg |

| D4 Repeatability | +/- 0.1 - 0.2 mm | +/- 0.01 - 0.02 mm | +/- 0.02 - 0.05 mm |

| D5 Drive | Electric AC servo | Electric AC servo | All-joint torque-sensing electric |

| Unit ASP | USD 80,000 - 200,000 | USD 15,000 - 45,000 | USD 25,000 - 65,000 |

| Market CAGR | ~7% (mature) | ~11% | ~23% (emerging) |

ASP estimates based on FANUC, ABB, Universal Robots, Epson public list prices and channel data. CAGR: MarketsandMarkets, Grand View Research, Precedence Research composite.

7 Chapter Conclusions

The Five-Dimensional Classification System reveals four strategic imperatives for market participants:

1. Kinematic configuration is no longer the sole competitive moat. As articulated robot hardware approaches commodity pricing (sub-USD 20,000 for 6-axis models from leading Chinese OEMs), differentiation is shifting to Dimensions II-V: specialized application software, precision tier, and intelligent drive systems.

2. The light-payload + ultra-precision intersection is the fastest-growing commercial white space, driven by semiconductor, medical device, and advanced electronics. No incumbent has established a dominant position in this quadrant.

3. The electric drive revolution is restructuring supply chains. The shift to all-electric architectures concentrates value in servo motors and precision reducers — components where Chinese suppliers (Inovance, Leadshine; Shuanghuan, ZD Reducer) are rapidly gaining share versus Japanese incumbents.

4. Food & beverage's 42% YoY installation surge in 2024 signals an under-analyzed expansion front. This sector's profile (delta and articulated, light-to-medium payload, IP67+ enclosures, +/-0.05-0.1 mm repeatability) represents a distinct specification cluster demanding targeted go-to-market strategies.

Data Sources: IFR World Robotics 2025 | MarketsandMarkets | Grand View Research | Precedence Research | GlobalInfoResearch

{kind=link}

Leave a comment