Executive Summary

Serve Robotics ended FY2025 as the operator of the largest autonomous sidewalk delivery fleet in the United States — 2,000+ robots across 20 cities. Full-year revenue reached $2.7M (+50% YoY), beating guidance, with Q4 alone surging 400% year-on-year to $0.9M as the fleet hit commercial density in core markets. The company closed the year with $260M cash and guides ~$26M in revenue for 2026.

The core business logic is straightforward: replace a $8–10 per-order human courier trip — typically covering just 2.5 miles — with a robot that costs under $1 per delivery at scale. Whether that threshold is achievable in practice, and when, is the defining question for the platform. FY2025 established the fleet and the operational data pipeline to start answering it. Four strategic acquisitions have simultaneously pushed Serve into hospital logistics and Physical AI infrastructure, transforming it from a delivery operator into a multi-domain robotics platform.

$2.7M FY2025 Revenue ↑ 50% vs $1.8M FY2024 | +400% Q4 YoY Growth Q4 revenue: $0.9M | $(101M) FY2025 Net Loss vs $(39.2M) FY2024 | $260M Cash & Securities Year-end 2025 |

2,000+ Robots Deployed Largest U.S. sidewalk fleet | 1.8M+ Total Deliveries Sidewalk + Hospital to date | 99.8% Completion Rate Industry-leading | ~$26M FY2026 Target ~10× FY2025 |

Why Now: Three Converging Forces

1. Edge AI Has Reached Commercial Viability

Five years ago, running real-time semantic segmentation, pedestrian prediction, and path planning on a $300 compute module was impossible. NVIDIA's Jetson Orin — which powers the Gen3 robot's autonomy stack — delivers up to 275 TOPS of AI performance at under 60W. Vision transformer architectures trained on real-world urban data now handle unstructured sidewalk environments with reliability that discrete rule-based systems never could. Serve's acquisition of Vayu Robotics (AI foundation models) reflects the sector-wide shift toward end-to-end learned autonomy replacing handcrafted perception pipelines.

2. Labor Economics Have Shifted Against Human Delivery

California's AB5 reclassification pressure, the state's $20/hr fast-food minimum wage, and rising gig platform insurance costs have structurally increased the cost of human last-mile delivery. Platforms like Uber Eats and DoorDash are under active margin pressure to reduce per-order fulfillment costs — making robot delivery not just a novelty but an economic necessity at scale. Serve's integration into both platforms means it captures demand directly from this pressure.

3. Q-Commerce Has Created the Right Order Profile

Post-pandemic consumer behavior locked in the expectation of sub-30-minute food delivery. The median U.S. food delivery covers 2.5 miles — a distance perfectly matched to a 11-mph robot with a 14-hour operating window. Urban order density in Serve's launch markets (LA, Miami, Chicago, Atlanta) provides the geographic concentration needed to keep robots utilised across multiple trips per hour rather than deadheading between orders.

Technology & Autonomy: Reality Check

What Level 4 Autonomy Means in Practice

Serve claims Level 4 autonomy for its sidewalk fleet — meaning the robot can complete its mission without human intervention under defined operational conditions (ODD: urban/suburban sidewalks, daylight and low-light, standard weather). In practice, Level 4 on a public sidewalk is meaningfully harder than Level 4 in a geofenced campus or controlled warehouse, because the environment changes unpredictably: cyclists cut across sidewalks, construction zones appear overnight, and pedestrian behaviour in dense urban environments is fundamentally non-deterministic.

Teleoperation Still Has a Role

Serve's acquisition of Phantom Auto — which provides ultra-low latency remote supervision technology (the Voysys platform) — signals that human oversight remains part of the operational model. This is not a weakness: the best-performing autonomous systems use teleoperation as a fail-safe and data collection mechanism rather than a crutch. Every supervisor intervention generates a labelled edge case that feeds back into the training pipeline. The 99.8% completion rate is impressive, but the operationally relevant question is what happens to the 0.2% — and Phantom Auto is the answer.

Real-World Operating Constraints

Weather: Gen3 handles −4°F to 113°F and heavy rain (vs Gen2's light rain only). Effective in most U.S. climates but limited in snow-heavy northern cities — relevant context for the planned NYC and Chicago expansion.

Vandalism & theft: Sidewalk robots in urban environments face tampering risk. Serve has not disclosed vandalism incident rates publicly, but robot bodies feature visible branding (Shake Shack, Little Caesars) which may deter some interference while increasing visibility.

Pedestrian & cyclist interaction: The Gen3's dual-camera array and LiDAR stack (Ouster sensors) handle most scenarios, but dense pedestrian events (street festivals, sidewalk closures) remain edge cases that push robots into supervised operation.

Speed vs. human couriers: At 11 mph max, a Gen3 robot is slower than a motivated bike courier (avg 15–18 mph in clear conditions) and significantly slower than a moped. The robot's advantage is consistency across 14-hour shifts, not peak speed.

Financial Snapshot

Revenue grew from $1.8M (FY2024) to $2.7M (FY2025), beating the company's own $2.5M guidance. Q4 2025 contributed $0.9M — one-third of the full year in a single quarter, driven by deploying ~1,000 robots in that period alone. Net loss widened from $39.2M to $101.4M, primarily reflecting four M&A transactions, the cost of scaling manufacturing from 100 to 2,000 robots via Magna International, and R&D on the Gen3 platform. The company carries $260M in cash — roughly 2.5 years of runway at current burn. FY2026 guidance is $26M revenue against projected non-GAAP operating expenses of $160–170M.

| Key Numbers | FY2024 | FY2025 | FY2026 Guide |

| Revenue | $1.8M | $2.7M | ~$26M |

| Net Loss | $(39.2M) | $(101.4M) | n/d |

| Cash (year-end) | — | $260M | — |

| Non-GAAP Opex | — | ~$103M | $160–170M |

| QoQ Delivery Growth | ~40%+ (since 2022) | ~40%+ | Target: maintain |

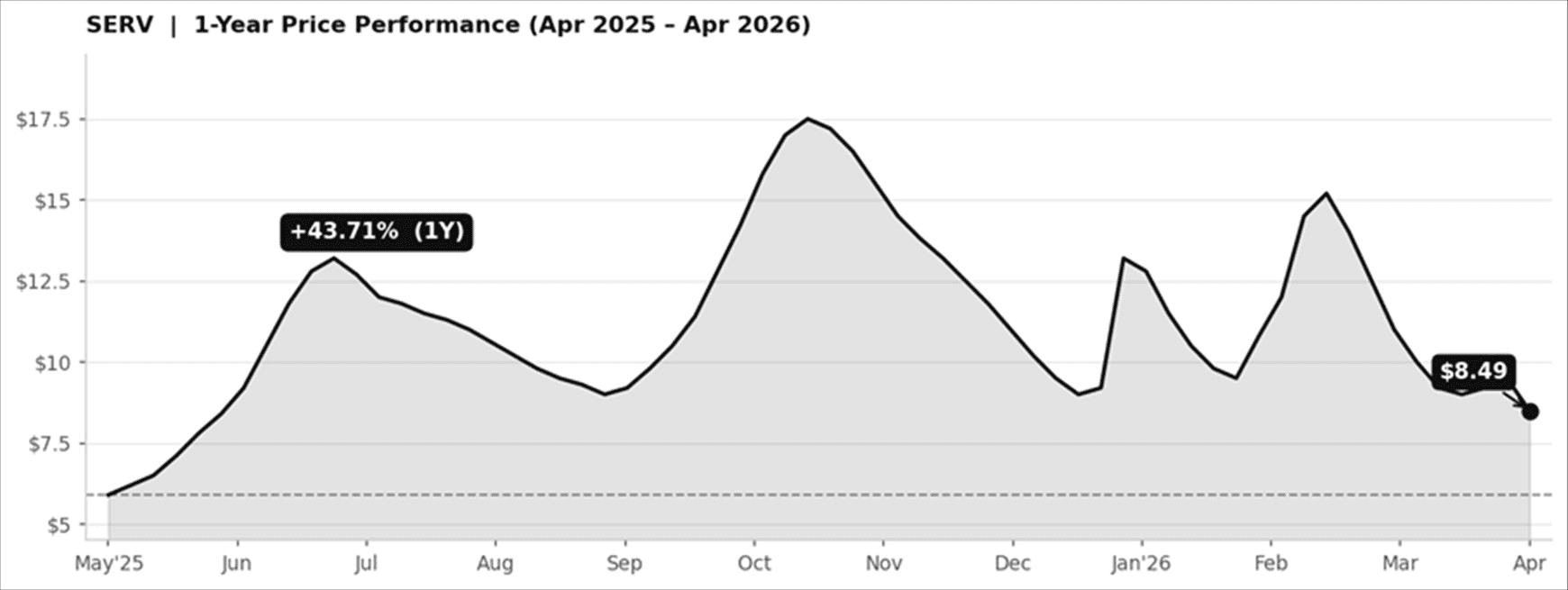

SERV: 1-Year Price Performance

SERV: $8.49 as of Apr 4, 2026 (+43.71% 1Y). Peak ~$17.50 in Oct 2025 on fleet scale milestones. Current pullback reflects FY2026 investment cycle overhang.

Competitive Landscape

Serve operates in an emerging sidewalk robotics market with a handful of meaningful players, each with distinct technology and business model trade-offs:

| Company | Autonomy Model | Fleet / Scale | Key Difference | Status |

| Serve Robotics | Level 4 + supervised | 2,000+ robots, 20 U.S. cities | Dual-platform (Uber+DoorDash); Physical AI multi-domain | Public (NASDAQ: SERV) |

| Starship Technologies | Semi-autonomous, campus-focused | ~1,000+ units, UK/US campuses & suburbs | Proven long-term ops; campus/suburban ODD; not city-scale | Private (VC-backed) |

| Coco Robotics | Teleoperation-heavy | ~100s of units, dense urban U.S. | Human-operated cooler robots; lower autonomy bar; high labour cost | Private; restructuring |

| Nuro | Full vehicle autonomy (road-based) | Small fleet, suburban U.S. | Road vehicles (not sidewalk); grocery/pharmacy focus; different regulatory path | Private (SoftBank-backed) |

The competitive read: Starship is the closest operational peer but has not scaled to city-level density or dual-platform integration. Coco's teleoperation-heavy model demonstrates the unit economics problem Serve is trying to solve — high human oversight costs erode the margin case. Nuro competes in a fundamentally different regulatory and physical environment (road vs. sidewalk), making them a contrast case rather than a direct rival. Serve's defensible advantage is its combination of fleet scale, operational data volume (~40% QoQ compounding since 2022), and platform lock-in with Uber Eats and DoorDash.

Strategic Moves: Four Acquisitions in 2025

CEO Ali Kashani executed four acquisitions targeting distinct layers of the autonomy stack — from perception models to hospital logistics:

| Acquisition | Layer | What It Adds |

| Vayu Robotics | AI Foundation Models | End-to-end physical AI models for indoor + outdoor autonomy; shifts Serve toward learned perception rather than handcrafted pipelines. |

| Phantom Auto | Connectivity / Supervision | Voysys ultra-low latency teleoperation; remote supervision as both safety net and continuous training data generator. |

| Diligent Robotics | Indoor / Healthcare | ~100 Moxi hospital delivery robots; 1M+ tasks across 25+ hospitals; ~$200K/facility/year recurring revenue. Indoor autonomy domain data. |

| Vebu | Kitchen / QSR Integration | Kitchen automation deepening restaurant brand partnerships and merchant on-ramp for delivery. |

FY2026: What to Watch

The $26M revenue target — roughly 10× FY2025 — hinges on three operational levers:

Utilisation ramp: 2,000 deployed robots generating more orders-per-robot-per-day as neighbourhood density increases. This is the primary revenue driver without adding new hardware capital.

Diligent Robotics revenue (~$7M): Hospital contract ramp is the most predictable component — recurring, contracted, and not weather-dependent.

International expansion: New York, Sydney, Vancouver targeted in 2026. Each new market adds data diversity but also regulatory and operational overhead.

The autonomy metric worth tracking is not just the completion rate (already at 99.8%) but the intervention rate — how often and under what conditions does the Phantom Auto supervision layer get invoked? That number, if disclosed, would be the most revealing indicator of where the platform sits on the path to genuine unsupervised Level 4 operation in dense urban environments.

Disclaimer: For informational purposes only. Not financial or investment advice. All figures sourced from Serve Robotics public filings, press releases, and March 2026 Investor Presentation. Forward-looking statements subject to material risks; see company SEC filings.

{kind=link}

Leave a comment