FlexQube AB (FLEXQ)

Order Flow, Stock Performance & Market Cap Growth

12-Month Analysis | April 2025 – March 2026

Company Snapshot

| Full Name | FlexQube AB (publ) |

| Ticker (Stockholm) | FLEXQ — Nasdaq First North |

| Ticker (Frankfurt) | A1Y — Deutsche Boerse |

| Founded | 2010, Mölndal (Gothenburg), Sweden |

| HQ | Gothenburg, Sweden; subsidiaries in USA, Mexico, Germany, UK |

| Employees | ~42 (as of early 2026) |

| Revenue (TTM) | SEK 113.56M (~USD 10.5M) |

| Market Cap | ~SEK 138–148M (March 2026) |

| 52-Week Range | SEK 4.66 – SEK 16.25 |

| Current Price (Mar 2026) | ~SEK 9.78–12.65 |

| Analyst Target (2026) | SEK 25.00 (consensus, +127% vs ~SEK 11) |

| Primary Markets | North America (~55% of revenue), Europe |

Product Portfolio & Technology

FlexQube operates at the intersection of modular manufacturing engineering and industrial robotics, offering a three-tier product stack that spans manual cart systems, line-following AGVs, and fully autonomous mobile robots (AMRs). The unifying principle across all tiers is FlexQube's patented building-block modular architecture: a small set of standardized components that can be configured, reconfigured, and scaled to virtually any intralogistics use case.

Tier 1 — Mechanical Cart & Tugger Train Systems

The company's original and still highest-revenue product line consists of customizable industrial carts assembled from standardized structural blocks. Product types include pallet and container carts, shelf and flow carts, hanging carts, mother-daughter solutions, kit carts for assembly-line sequencing, and rotating fixtures. The LiftRunner tugger train system enables one tractor unit to pull a train of loaded carts through a facility, replacing forklift traffic on high-frequency routes. Carts are designed using FlexQube's Design4All CAD library or through the DesignOnDemand service, where FlexQube engineers produce custom configurations against assembly-line principles.

Tier 2 — eQart Line-Following AGV

The eQart is a motorized, line-following automated guided vehicle that follows magnetic tape or optical guidance strips pre-laid on the factory floor. It occupies the middle tier between fully manual carts and fully autonomous AMRs — suitable for high-repetition, fixed-route material flows where infrastructure simplicity and low cost are priorities. The eQart shares the same modular load-carrier ecosystem as the Navigator AMR, meaning customers can migrate from manual to line-following to autonomous operation on the same cart fleet.

Tier 3 — Navigator AMR System (Core Growth Driver)

The FlexQube Navigator is the company's proprietary Autonomous Mobile Robot, and the primary driver of the order acceleration seen across the past 12 months. The Navigator is a "non-load-carrying" AMR: rather than carrying materials directly, it docks to and navigates motorized load carriers via a standardized coupling interface. The coupling transfers both power and control data to the motors on the load carrier, enabling the Navigator to drive carts of radically different sizes, shapes, and payload capacities without modification to the AMR itself.

Navigation and fleet management run on BlueBotics' ANT software — a proven autonomous navigation stack used across hundreds of industrial deployments globally. Wireless inductive charging (via Wiferion) eliminates contact-based charging downtime. The Navigator won the RBR50 Innovation Award in 2022 and has since accumulated an extensive patent portfolio across the US, Europe, Canada, China, Turkey, and multiple pending applications in Japan, South Korea, Mexico, and India.

Patent Portfolio — AMR Navigator (as of March 2026)

FlexQube has been granted at least 6 patents for the Navigator AMR system and has 19+ further applications pending globally. Key granted jurisdictions include the United States (valid to 2041), EU/EES, UK, Canada, China, and Turkey. The October 2025 European grant of the conceptual-level patent — protecting the core idea of a standardized AMR docking to a wide range of motorized load carriers via a standardized interface — is particularly significant, as it covers the platform principle rather than merely specific implementation technologies. This mirrors the protection model seen in robotic-arm end-effector ecosystems.

Market Context

The global automated material handling (AMH) robot market was valued at approximately USD 2 billion in 2022 and is projected to reach USD 10 billion by 2032, representing a compound annual growth rate of approximately 17.9%. FlexQube is positioned as a mid-market, implementation-lean alternative to large AMR platforms: its "one AMR, many carriers" model reduces both capital expenditure and operational complexity for customers running varied material flows — a pain point acute in automotive, e-commerce, and heavy manufacturing. The company sells to over 1,000 customers across 38 countries, with significant penetration into Fortune 500 manufacturers in automotive, electric vehicles, online retail, heavy trucks, aerospace, and defense sectors.

Order Flow: April 2025 – March 2026

The 12-month period under review saw FlexQube execute its most consequential commercial acceleration since the company's founding. Order announcements followed a clear escalation arc: from individual mid-five-figure US cart orders in spring 2025, through the breakthrough of a flagship US e-commerce pilot program in late summer and autumn, culminating in the single largest order in the company's history — a USD 13 million contract announced in March 2026.

| Date | Event | Value | Category / Note |

|---|---|---|---|

| Nov 2024 | Texas cart order (HVAC/heating customer) | ~USD 390K | Mechanical — repeat customer |

| Apr 2025 | Texas cart order (energy/HVAC) | ~USD 470K | Mechanical — repeat customer |

| Jun 2025 | US car manufacturer — tugger train | ~USD 0.9M | Largest N. America order in 3 years |

| Aug 2025 | Tennessee manufacturer — custom carts | ~USD 0.3M | Mother-daughter ergonomic systems |

| Oct 2025 | US customer pilot (new division) | ~USD 270K | Navigator AMR — new project/division |

| Oct 2025 | US customer — major potential project pilot | TBD | Cart + AMR expansion pathway |

| Oct 2025 | European patent granted (conceptual AMR) | IP event | Platform-level protection |

| Nov 2025 | US e-commerce — follow-up order | ~USD 1.3M | Pilot program total >USD 3M |

| Nov 2025 | South Carolina tugger train systems | ~USD 0.74M | Existing US customer |

| Dec 2025 | European fashion retailer pilot (Poland) | SEK 1.1–2M | Navigator AMR — Q2 2026 pilot |

| Jan 2026 | US e-commerce follow-up #1 | ~USD 455K | Q1 2026 delivery |

| Jan 2026 | US e-commerce follow-up #2 | ~USD 430K | Q1 2026 delivery |

| Feb 2026 | Mexico automotive supplier — Navigator AMR | ~SEK 2.5M | First project + framework agreement |

| Mar 2026 | US e-commerce MEGA ORDER | ~USD 13M | Largest order in company history |

Note: Values are as announced. Some orders denominated in SEK converted at approximate prevailing rates. The November 2024 order is included as the 12-month starting baseline.

Cumulative Order Value Commentary

The USD 13 million March 2026 order from one of the world's largest US-based e-commerce and logistics companies is not an isolated event — it is the capstone of a structured pilot-to-deployment relationship that FlexQube has systematically built since August 2025. The sequence ran: initial pilot → additional pilot in a different division → two follow-up orders totaling ~USD 1.75M → the USD 1.3M follow-up (cumulative pilot program exceeding USD 3M by November 2025) → and finally the scale order of USD 13M, which represents one of the largest single AMR system deployments disclosed by any player in the mid-market intralogistics segment. Including all disclosed orders across the 12-month window, FlexQube's aggregate announced order value approaches approximately USD 18–19 million — a figure that dwarfs its trailing twelve-month revenue of approximately USD 10.5M (SEK 113.56M), and points toward a material step-change in the company's revenue trajectory heading into 2026 and 2027.

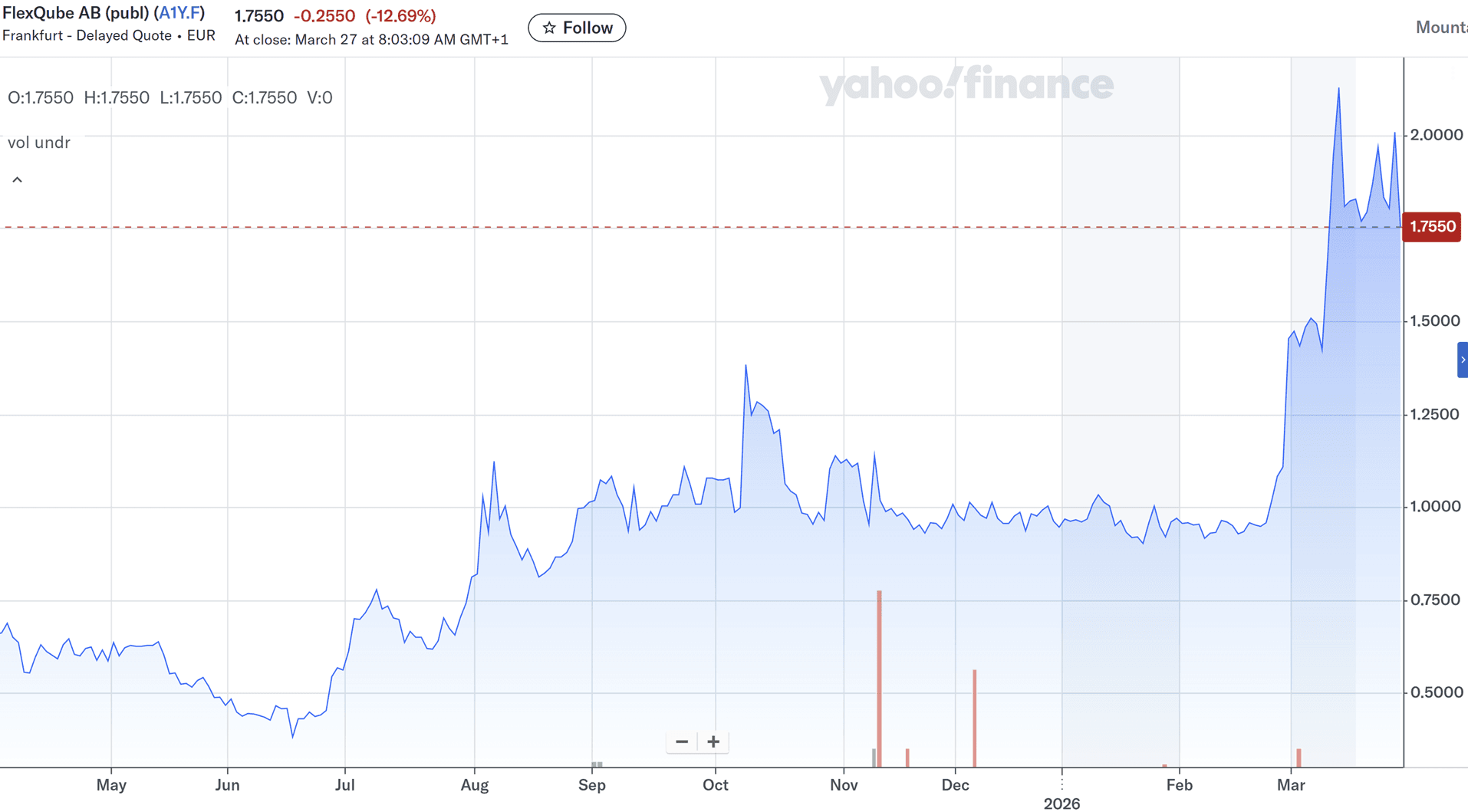

Stock Performance: April 2025 – March 2026

The FLEXQ share price (Stockholm: FLEXQ / Frankfurt: A1Y) charted one of the most dramatic recovery arcs among small-cap industrial robotics equities on the Nasdaq First North over the period under review. The following narrative reconstructs the key inflection points based on confirmed data and order announcement dates.

Phase 1 — Capitulation (April – June 2025)

The stock entered the review period under sustained selling pressure inherited from a difficult 2024 in which the company burned cash while scaling its AMR development and pilot programs without yet achieving the commercial validation needed to reassure investors. FLEXQ reached its all-time low of SEK 4.66 on 16 June 2025 — a level that implied a market capitalisation of approximately SEK 62–65M against trailing revenues of SEK 113M, suggesting the market was ascribing near-zero terminal value to the AMR business. At this floor, the stock traded at a Price/Sales ratio of roughly 0.55x — among the lowest observed for any listed AMR-adjacent company globally.

Phase 2 — Pilot Validation & Recovery (July – October 2025)

The inflection began with the June 2025 announcement of a USD 0.9M tugger-train order from a US car manufacturer — the single largest order in three years — signalling that FlexQube's mechanical business was returning to form. The August Tennessee order followed, and critically, the October 2025 disclosure of two concurrent Navigator AMR pilots at the same major US e-commerce customer (different divisions) catalysed a sharp re-rating. The simultaneous granting of a key European patent covering the conceptual AMR platform principle reinforced the IP moat narrative. By late October 2025, the stock had recovered to the SEK 10–12 range, representing a roughly 115–158% gain from the June low.

Phase 3 — Momentum Build (November 2025 – January 2026)

The November 2025 follow-up order of USD 1.3M — pushing the total US pilot program beyond USD 3M — sustained buying interest. The stock traded in the SEK 10–16.25 range through this period, with the 52-week high of SEK 16.25 likely touched in this window as institutional awareness of the US e-commerce customer relationship grew. The market cap reached approximately SEK 218M at the peak — more than triple the June 2025 floor. Two further follow-up orders from the same US customer were announced simultaneously in January 2026, totalling approximately USD 885K, confirming the deployment was scaling toward production.

Phase 4 — Consolidation & Reloading (February – March 2026)

Following the peak, FLEXQ pulled back to the SEK 10–13 range as investors assessed execution risk on the growing order backlog and the pending full-year results (scheduled 22 April 2026). The February 2026 Navigator AMR framework agreement with a Mexican automotive supplier — the first in the region to include a multi-facility framework — added geographic diversification to the order story without moving the stock materially. The March 2026 USD 13M order announcement constitutes the most recent and most powerful catalyst in the series, and market reaction to this event (likely occurring at or just after the data cut of this analysis) is expected to be significant.

Market Cap Growth Analysis

The market capitalisation trajectory across the 12-month window is best understood in three quantitative anchors:

| Period | Share Price (SEK) | Implied Market Cap | Catalyst |

|---|---|---|---|

| Jun 16, 2025 (Low) | 4.66 (ATL) | ~SEK 62M | All-time low; pre-pilot results |

| 52-Wk High (~Nov/Dec 2025) | 16.25 | ~SEK 218M | US pilot program scaling |

| Mar 29, 2026 (Current) | ~9.78–12.65 | ~SEK 138–170M | Post-consolidation; pre-USD 13M |

From its June 2025 all-time low, FLEXQ delivered a peak intra-period gain of approximately +249% to SEK 16.25, and remains approximately +110–172% above the low on a sustained basis as of late March 2026. On a trailing 12-month basis against the prior year-end, the stock has returned approximately +14% (Stockopedia) — a figure that understates the volatility of the round trip, and which will be revised significantly upward once the market fully prices the USD 13M order. The analyst consensus target of SEK 25 implies an additional ~127% upside from current prices, a spread that reflects both the genuine optionality in the US e-commerce account and the execution risks inherent in a 42-person company managing an order backlog that has ballooned in under 12 months.

Investment Perspective

Bull Case

The USD 13M e-commerce order is a blueprint, not a ceiling. The customer is one of the world's largest logistics operators with hundreds of warehouse facilities globally. If FlexQube successfully executes this deployment, the framework could generate repeat orders that individually exceed the company's current annual revenue.

The Navigator AMR's 'one robot, many carriers' architecture is genuinely differentiated and broadly patented through 2041. Competing AMR platforms require dedicated robots per application; FlexQube's model reduces capex for customers running mixed-material flows, which is the majority of complex manufacturing and e-commerce environments.

The diversification of the order book into European retail (Poland pilot), Mexican automotive (first framework agreement in region), and US manufacturing across multiple verticals reduces concentration risk meaningfully versus 12 months ago.

Analyst consensus target of SEK 25 represents a Price/Sales multiple of approximately 3.3x on trailing revenues — modest for a high-growth industrial robotics name with a proprietary platform and a confirmed Fortune 500 deployment at scale.

Risk Factors

Execution risk: FlexQube employs ~42 people. Delivering, installing, and commissioning a USD 13M AMR deployment at a major logistics operator is operationally demanding and may require rapid headcount or supply-chain scaling.

Balance sheet: Total Debt/Equity stands at approximately 220% (TTM), and the company continues to post net losses (net income approximately -SEK 31.75M TTM). The order book expansion must convert to cash-generative revenue quickly to avoid a dilutive equity raise.

Customer concentration: The US e-commerce customer appears to represent a very substantial share of the near-term pipeline. A delay, scope reduction, or cancellation of scale orders would have an outsized impact on both revenue and sentiment.

Macro: Tariff uncertainty and potential softness in US industrial capital expenditure could slow deployment timelines at customer sites, particularly in the automotive sector.

Editorial Summary

FlexQube enters Q2 2026 as one of the most compelling small-cap turnaround stories in European industrial robotics. Twelve months ago the company was trading at an all-time low, burning cash, and carrying an AMR product line that the market was effectively valuing at zero. Today, it holds the largest order in its 14-year history, a Europe-wide patent protecting its platform concept, and a growing footprint in e-commerce, automotive, and retail logistics across three continents. The gap between the stock's current valuation and the analyst target is wide, and the USD 13M order is the kind of inflection-point event that tends to close such gaps — but only if execution meets the ambition of the order book. For robotics investors with a 12–18 month horizon and tolerance for small-cap liquidity risk, the FLEXQ thesis has rarely been cleaner.

This article is for editorial and informational purposes only. It does not constitute investment advice. Past stock performance is not indicative of future results. RobotToday does not hold positions in any securities discussed.

{kind=link}

Leave a comment