Laser weeding is shifting from a niche sustainability tool into a core layer of autonomous farming. The market is undergoing a structural break: AI-powered, chemical-free, per-plant precision is replacing decades of blanket herbicide spraying.

Two companies now anchor opposite ends of the global competition—Carbon Robotics in the U.S. and HGTech in China—while open-source challengers and Big Ag incumbents are forming a fast-moving competitive perimeter.

1. Carbon Robotics — The Uncontested Global Leader

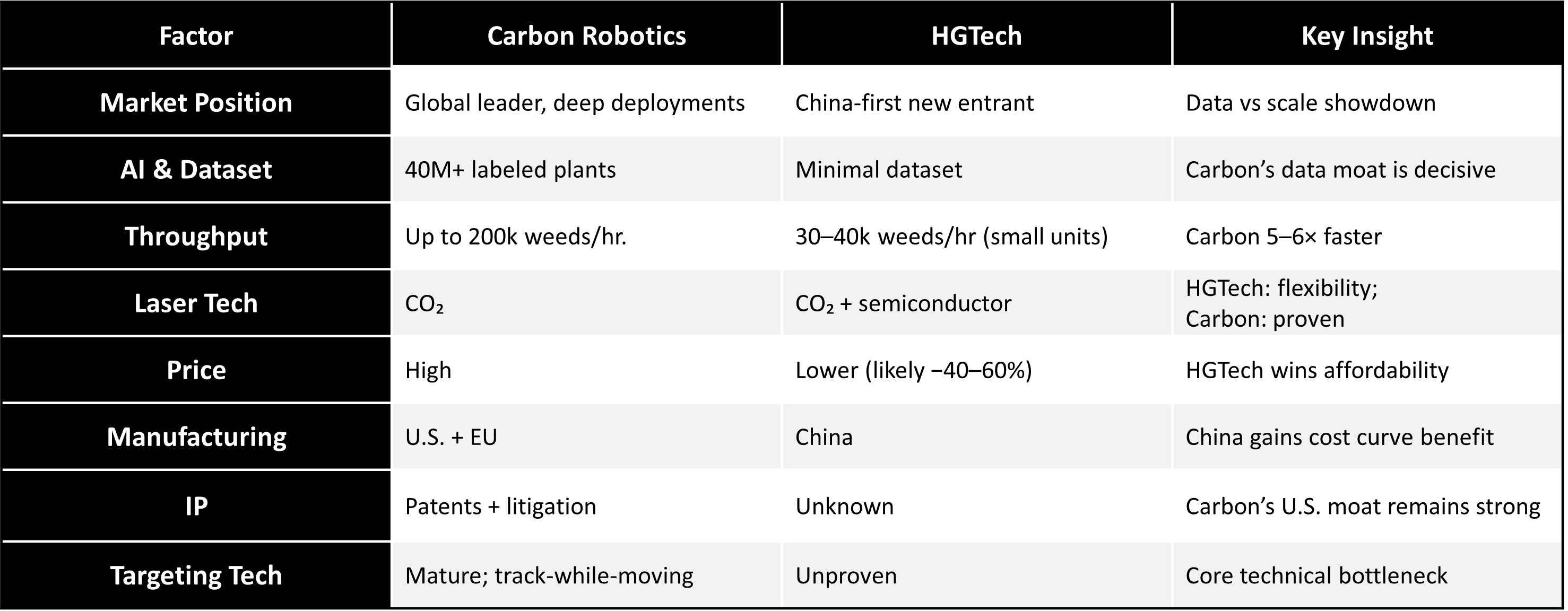

Carbon Robotics is the world’s most advanced and commercially proven laser-weeding platform. With deployments in 14 countries and a cumulative 40M+ labeled plant dataset, Carbon owns the only large-scale agricultural per-plant AI model in actual production.

A recent Series D-2 extension ($20M) brings total funding to an estimated $177–255M, with resources now flowing into a third undisclosed farm robot—signaling ambitions beyond weeding.

Technology & Product: G2 LaserWeeder

- Precision: Sub-millimeter laser targeting, 10ms recognition cycle

- Throughput: Up to 200,000 weeds/hour (towed G2)

- AI Model: “Large Plant Model” trained on 3 continents; continuous learning

- Portfolio: Five modular sizes (8–40 ft), 25% lighter

- Operations: 2 acres/hour towed, or 15–20 acres/day autonomous

- Manufacturing: U.S. + Netherlands (tariff-resilient dual supply chain)

Strategic Advantages

- Data Moat: No other company approaches Carbon’s real-world dataset scale

- Target-While-Moving: Carbon’s proprietary tracking system is widely regarded as the hardest technical problem in laser weeding

- Customer Control: Direct sales, no dealerships—tight feedback loop

- Patent Defense: Already won a preliminary injunction against L&A in the U.S.

Challenges

• High unit price limits penetration into mid-sized farms • Chinese entrants pose long-term price-driven disruption risks • Mechanical weeding still dominates <100-acre operations

Carbon today resembles the Tesla of precision weeding: expensive, technologically superior, and years ahead in real-world training data.

2. HGTech — China’s Technological Challenger

HGTech is leveraging decades of industrial laser manufacturing to enter agricultural robotics. Its debut at CIAME 2025 marked the most complete Chinese laser-weeding lineup to date—designed for China’s fragmented fields, cooperative farms, and deep price sensitivity.

Product Matrix: Nongfu & Shennong Series

Nongfu A Series (Small to Medium Farms)

- Lasers: 3–4 CO₂ lasers

- Throughput: 30,000–40,000 weeds/hour

- Operation: 8–15 acres/day (electric) or 15–20 acres/day (hybrid)

- Energy Cost: <5 RMB/hour

- Use Case: 100-acre plots, orchards, greenhouses

Shennong H Series (Large-scale Agricultural Operations)

- Modular: 4–16 laser units

- Width: 2.2–8.8m

- Required Power: 120+ HP tractors

- Throughput: Up to 160 acres/day

- Integration: Real-time farm management data sync

Technical Differentiation

- Tri-laser compatibility: CO₂ mid-IR, semiconductor near-IR, semiconductor blue—unique flexibility

- Environmental Hardening: Dustproof, fog-resistant, light-rain operations

- Organic Compliance: GB/T19630

- Cost Advantage: Far lower purchase price + <$1/hour operations

Strategic Weaknesses

- AI gap: No large-scale plant datasets; training is early stage

- No global deployments: Performance claims lack third-party validation

- IP exposure: Entering U.S./EU risks litigation

- Service readiness: Export after-sales infrastructure is unclear

HGTech is executing a classic China-first, cost-optimized, fast-scale strategy. If they solve plant-model training and field stability, they could become the Huawei of laser weeding in Asia.

3. Other Meaningful Competitors

Laser Weeding

- Laudando & Associates (L&A) Open-sourced entire laser-weeding stack (AGPL + CERN OHL) after losing a U.S. injunction. This may seed Indian/Southeast Asian clone manufacturers.

Mechanical / Herbicide Precision Weeding

- Naïo Technologies (France) – Dino/Oz robots, strong EU farming base

- FarmWise (U.S.) – Mechanical AI weeding

- ecoRobotix (Switzerland) – 95% herbicide reduction

- Stout Industrial (U.S.) – Smart cultivator vision system

- Small Robot Company (UK) – Per-plant electric robots

Big Ag Integrations

- John Deere (Blue River Technology) – “See & Spray”

- Aigen – Solar-powered autonomous row-crop weeder

The practical reality: mechanical weeding still wins cost-per-acre for small farms, laser wins precision and chemical elimination for medium-large farms.

4. Comparative Analysis (RobotToday Condensed Edition)

5. Market Outlook (2025–2032)

2025–2027: Regional consolidation The laser-weeding market consolidates geographically. Carbon Robotics holds its lead in the U.S. and Europe through mature deployments and the largest per-plant dataset, while HGTech scales rapidly in China on cost and domestic market access. Mechanical weeding remains competitive for farms under 100 acres due to lower capital and service costs.

2028–2030: First commoditization cycle As Chinese and Southeast Asian manufacturers acquire laser system capabilities, hardware costs fall by an estimated 30–40%. Laser weeding moves from a premium solution to a viable option for mid-sized farms, marking the industry’s mainstreaming phase.

2030–2032: Standardization and bifurcation Per-plant autonomous weeding becomes standard for farms over 100 acres. The market clearly bifurcates: Carbon Robotics dominates premium Western and high-value crop markets, while HGTech leads in China and other price-sensitive regions. L&A’s open-source release may further compress global price floors.

Long-term drivers Competitive advantage shifts from hardware to data scale, target-while-moving stability, and service uptime. Tighter herbicide regulations accelerate adoption across all major markets.

6. Strategic Conclusions for RobotToday Readers

Carbon Robotics remains the benchmark for precision laser weeding, anchored by unmatched per-plant AI models and proven field reliability. High pricing limits near-term penetration, but its multi-robot roadmap and IP strategy secure a durable premium-market moat.

HGTech is the strongest challenger in Asia. Its cost-optimized systems align well with fragmented farmland and emerging markets. The key gap is not hardware, but AI data depth and long-term field validation, alongside exposure to Western patent barriers.

The major wildcard is L&A’s open-source laser-weeding stack. If adopted by Indian or ASEAN manufacturers, sub-$20,000 systems could emerge, rapidly commoditizing hardware. In that scenario, differentiation shifts decisively to software—model accuracy, continuous training pipelines, and cloud-based agronomic intelligence.

{kind=link}

Leave a comment