1. Company Overview and History

Galaxis Tech (Zhejiang Galaxis Technology Group Co., Ltd.) traces its origin to Wuxi Galaxis Technology, founded in June 2014. The company was formally incorporated in October 2016 and converted into a joint-stock company in July 2021. It is headquartered in Jiaxing, Zhejiang.

The company was founded by Gu Chunguang (Chairman and CEO, former CTO of Jointown Pharmaceutical Group and ex-McKinsey & Company consultant) and Dr. Yang Yan.

Key milestones include:

2014: Launch and commercialization of first-generation MSR (multi-directional shuttle robot)

2017: Acquisition of Hubei Galaxis Tongda; introduction of MK high-speed lifts

2019: Establishment of AI research institute; launch of AMR and RCS systems; start of overseas expansion

2022: Release of VFR narrow-aisle forklift robot series

2024: Launch of VFR-CC series

The company completed six funding rounds, with post-money valuation rising from RMB 82 million to RMB 3.5 billion. Strategic investors include SF Holding, China Merchants Group, and Jointown Pharmaceutical Group.

Galaxis focuses on three core intra-logistics functions: storage, sorting, and handling. It has delivered over 1,600 projects across 29 industries, serving 861 customers in 19 countries, with an order backlog of approximately RMB 2.2 billion.

2. Products and Technology

Galaxis positions itself as a full-stack robotics provider integrating hardware and software across logistics workflows. It ranked fifth among China’s intra-logistics robotics companies by 2024 revenue (market share ~1.6%).

Core product lines

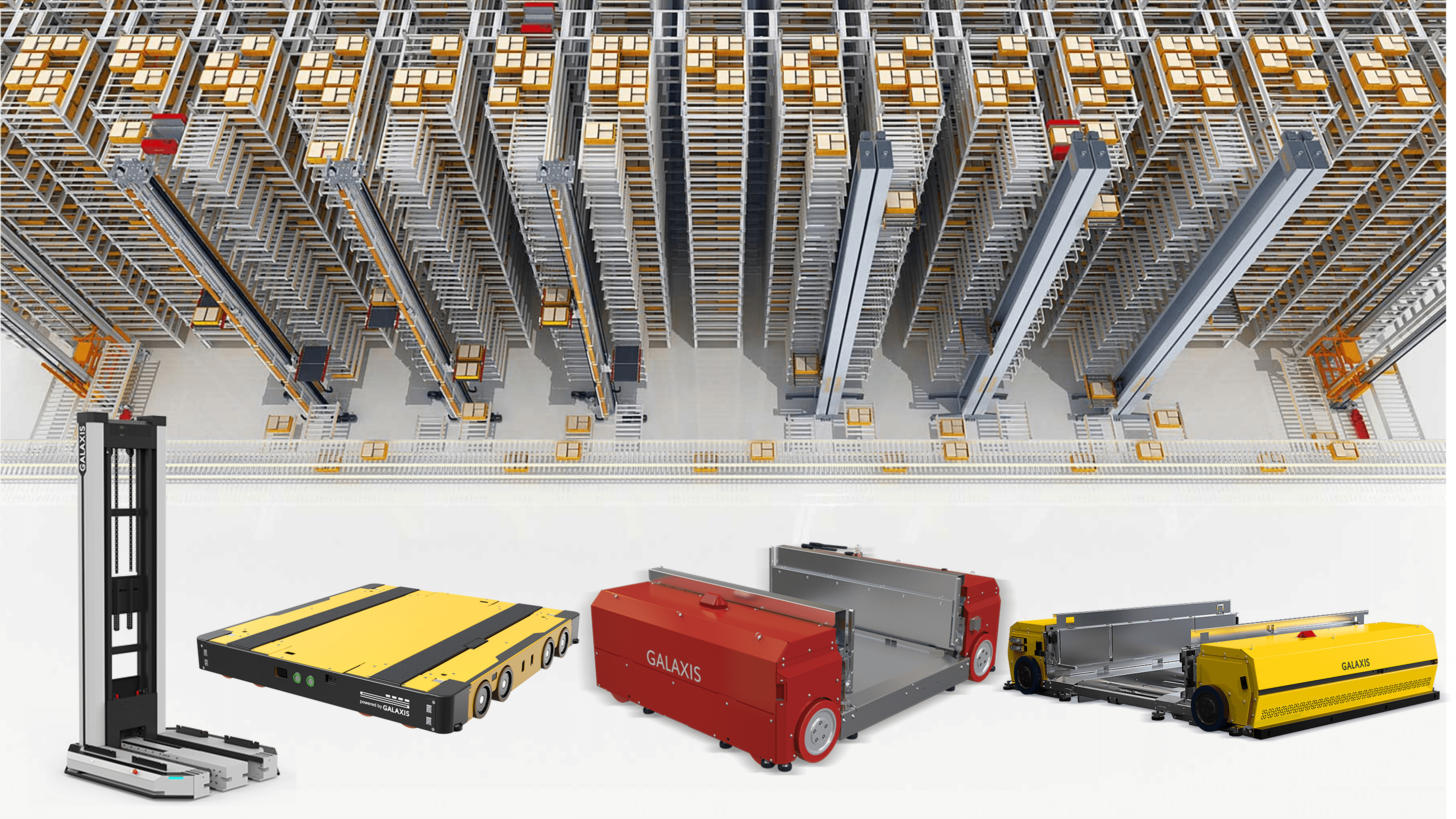

MSR (Multi-directional Shuttle Robots):

Enable bin/pallet movement across aisles and floors. Accuracy ±1–2 mm, speed up to 5.0 m/s, payload up to 1,500 kg. Designed for high-density storage and “goods-to-person” systems.AMR (Autonomous Mobile Robots):

Includes VFR narrow-aisle forklift robots (minimum aisle width ~1.65 m). Uses multi-sensor fusion and SLAM navigation. Suitable for manufacturing and dynamic warehouse environments.CSR (Conveying and Sorting Robots):

Vision-based recognition with real-time algorithms, supporting high-throughput sorting of standard and irregular items in e-commerce and industrial settings.

Software stack

WMS (Warehouse Management System)

WCS (Warehouse Control System)

RCS (Robot Control System)

The platform supports coordination of 1,000+ robots and high-volume order processing, with integration of digital twin and AI-based optimization for monitoring, routing, and predictive maintenance.

Key strengths

Full-scenario coverage across storage, transport, and sorting

High customization and modular deployment

358 domestic and 21 international patents

R&D team: ~29% of workforce; cumulative R&D spend ~RMB 290 million (2022–2025 YTD)

3. Financial Performance

Revenue shows recovery after a dip, with continued growth in 2025 YTD, while the company remains in an investment phase.

| Period | Revenue (RMB bn) | Gross Margin | Net Loss (RMB bn) | Net Liabilities |

|---|---|---|---|---|

| 2022 | 6.57 | 15.7% | 2.10 | 6.45 bn |

| 2023 | 5.51 | 16.6% | 2.42 | 8.94 bn |

| 2024 | 7.21 | 15.7% | 1.78 | 10.66 bn |

| 2025 (9M) | 5.52 | 16.6% | 1.34 | 11.96 bn |

Revenue is primarily driven by robot and system sales, supplemented by services. Losses are linked to R&D, capacity expansion, and share-based compensation.

Manufacturing is split between Jiaxing (MSR/AMR) and Wuhu (CSR). About 92.5% of revenue is from mainland China, with gradual international expansion.

4. IPO Details and Use of Proceeds

Offering: 36.8 million H shares (10% Hong Kong public, 90% international)

Offer price: HKD 16.66 (near lower end of range)

Net proceeds: ~HKD 556 million

Oversubscription:

Hong Kong public tranche: ~2,153x

International tranche: ~3.37x

Use of proceeds:

24.5% product upgrades

20.5% core technology (AI, digital twin)

25.0% capacity expansion

20.0% global market development

10.0% working capital

5. First-Day Trading Performance (March 24, 2026)

Opening price: ~HKD 32.2 (+~96%)

Market cap: ~HKD 14.0 billion

Grey market gain: >80% prior to listing

The strong debut reflects demand for exposure to logistics robotics, combined with sector growth expectations and backing from industrial investors.

6. Outlook and Risks

The IPO marks a transition from technology-led growth to capital-supported expansion. With a backlog of ~RMB 2.2 billion and broad industry exposure, the company is positioned to scale, particularly in manufacturing, e-commerce, and pharmaceuticals.

Key risks include:

Losses and margin pressure

Cyclical demand in downstream industries

Increasing competition in robotics and automation

Execution risks in overseas expansion

Potential volatility due to concentrated shareholding

Overall Assessment

The listing aligns with expectations given sector positioning, investor base, and order visibility. Longer-term performance will depend on execution, margin improvement, and international growth.

{kind=link}

Leave a comment