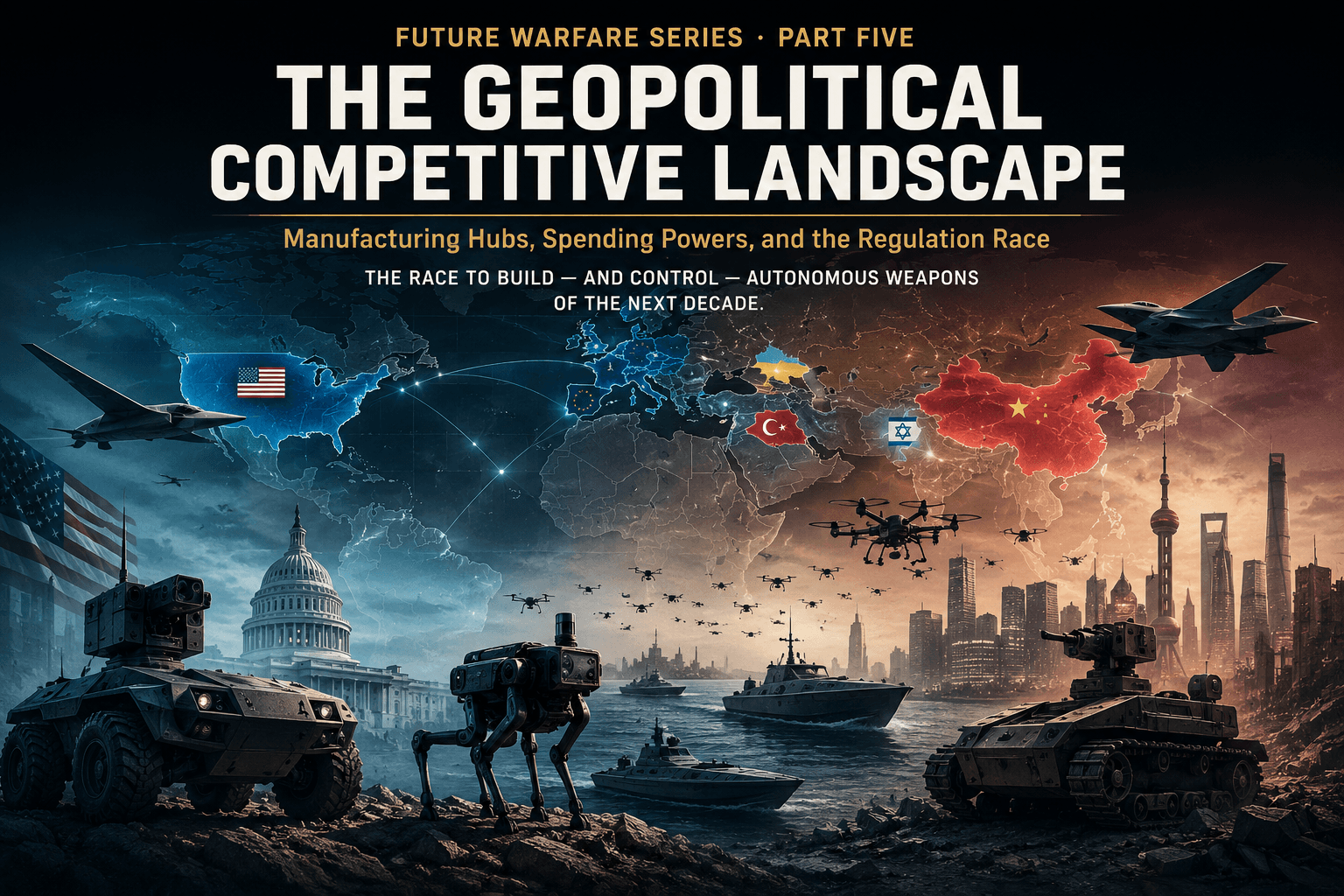

Military robotics is no longer a U.S.-centric story. Global defence spending crossed $2.75 trillion in 2026; defence-tech VC hit a record $49.1 billion in 2025; and a multipolar robotics order is crystallising in real time — with China’s 15th Five-Year Plan institutionalising civil-military fusion, Europe’s €381 billion defence budget financing its own AI champions, and Turkey and Israel reshaping the export market with affordable, combat-proven systems. Part Five maps the country-by-country competitive landscape, the collapsing regulation race, and the investment forces reshaping who builds — and who controls — the autonomous weapons of the next decade.

Introduction

A $2.75 Trillion Market, Seven Competing Visions

Global defence spending reached $2.75 trillion in 2026 — the highest level ever recorded, projected to reach $4.26 trillion by 2035. Defence-tech VC hit $49.1 billion in 2025, nearly doubling year-on-year and producing ten new defence-tech unicorns. EU member states spent a record €381 billion, crossing 2 percent of GDP for the first time. At the June 2025 NATO Summit in The Hague, allies committed to 5 percent of GDP by 2035 — potentially lifting European spending toward €800 billion annually. The country profiles below are not a catalogue of capabilities. They are a map of seven competing visions of what military autonomy is for, who should build it, and who gets to govern it.

Sources: StartUs Insights Defence Industry Report 2026; McKinsey European Defence Dashboard, February 2026; NATO Hague Summit Declaration, June 2025

I. Country Profiles: Seven Competitive Visions

🇺🇸 The Spender: United States Dominant in integration — racing to close the execution gap

The U.S. defence budget reached ~$967 billion in 2024 (3.38% of GDP); the Pentagon has set a $1 trillion target for 2026. Equity investment in defence tech nearly tripled to $14.2 billion in 2025. The architecture is increasingly software-first: Anduril ($30.5B valuation, Series G June 2025, advanced talks at ~$60B), Saronic ($4B, building a Louisiana shipyard), and Shield AI ($5.3B, USAF CCA Fury contract) are reshaping who supplies the Pentagon. The structural risk is execution: Replicator delivered hundreds where thousands were promised; the RCV was cancelled; the Orchestrator Challenge is a six-month sprint to build swarm command software the procurement system could not produce organically. China’s civil-military fusion is an ecosystem mandate. America’s is still a procurement experiment.

🇨n The Intelligentizer: China Leading in volume, AI velocity, and the whole-of-nation diffusion model

China’s advantage is not individual platform sophistication — it is a diffusion model: routing commercial AI (DeepSeek, Unitree robot dogs, DJI components) through Military-Civil Fusion procurement into fielded PLA applications faster and cheaper than any Western acquisition process allows. The 15th Five-Year Plan (2026–2030), finalising at the March 2026 NPC, institutionalises MCF as the path to an ‘intelligentized’ PLA by 2035. A Georgetown CSET analysis of 2,857 PLA AI contracts found that most suppliers are now civilian companies — two-thirds founded after 2010. Specific capabilities: Norinco’s DeepSeek-powered P60 combat vehicle; the Jiutian drone mothership (first flight December 2025); a programme to field one million tactical UAS by 2026; and the Type 076 Sichuan LHD capable of launching fixed-wing aircraft via electromagnetic catapult. Risk: CSET researchers flag that AI decision-support is being used partly to compensate for PLA command fragility, not only tactical need — a potential escalation driver.

🇹🇷 The Exporter: Turkey Affordable, combat-proven, politically unrestricted

Turkey has done what no other middle power has managed: carved a dominant position in the global armed drone export market. Baykar’s TB2 is deployed in 30+ countries; the Kizilelma UCAV — potentially the first carrier-capable combat drone from a non-major power — is in test flights; STM’s Kargu-2 completed its first live-fire swarm test in January 2026 and has been exported to 10+ countries including a confirmed NATO member. Turkey’s formula — affordable, battle-tested across Libya/Karabakh/Ukraine/Syria, and politically unrestricted where Western arms controls would block sales — is structurally difficult for Western competitors to match. Risk: Turkish systems sold to non-NATO customers have appeared on both sides of Western interests; the Kargu-2’s 2020 Libya autonomous engagement remains the most legally significant LAWS moment in history, yet produced no binding international response.

🇮🇱 The Urban AI Pioneer: Israel World’s most advanced AI targeting testbed — and most scrutinised

Israel activated the world’s first operational 100 kW laser defence system — Iron Beam — in September 2025, achieving hard kills on drones and rockets at roughly $4 per engagement. IAI and Elbit’s loitering munitions and Rafael’s systems (Iron Dome, Harop) are in service with more militaries than any country outside the U.S. The Gaza conflict has made Israel simultaneously the world’s most advanced AI-assisted strike testbed and the most legally scrutinised. EU export control discussions explicitly reference Israeli AI targeting as a test case; if Gaza-derived standards are adopted by European or UN frameworks, Israeli and U.S. targeting AI exports could face restrictions that Chinese and Turkish competitors would not.

🇺🇦 The Innovator Under Fire: Ukraine Fastest R&D cycle in history — and the world’s most valuable combat dataset

Ukraine is simultaneously the world’s most active autonomous systems combat theatre, fastest-iterating drone manufacturer, and most consequential swarm AI testbed. Its defence-tech sector raised $129M+ in 2025 despite active conflict; 270+ companies now produce UGVs; 500+ manufacturers produce up to 200,000 FPV drones per month; Swarmer filed for a Nasdaq IPO in 2026. The strategic implication for NATO is profound: Ukraine’s battlefield data — held in Swarmer’s algorithms, 270+ UGV manufacturers’ design choices, and drone units’ tactical doctrine — is the most valuable real-world autonomous systems dataset on earth. Countries accessing it through Brave1, USAI contracts, and bilateral programmes gain combat-validated iteration no test range can replicate. Risk: systems shaped by active-combat pressures may have failure modes that only emerge in different operational environments.

🇪🇺 The Procurer: Europe From €218B to €381B in four years — building sovereign AI before the window closes

EU member states spent €381 billion on defence in 2025 — up 62.8% from 2020. Germany unlocked a €500 billion defence fund in March 2025; Poland is spending 4.12% of GDP, the highest in NATO. European defence VC grew from €200 million in 2021 to €2.6 billion in 2025 — a thirteen-fold increase. The centrepiece is Helsing (valued at €12 billion after its June 2025 Series D), which has integrated its Centaur AI into the Eurofighter and Gripen, contracted HX-2 strike drones to Ukraine, unveiled the CA-1 Europa autonomous UCAV (first flight 2027), and tested its AI in a live dogfight against a human pilot — the first publicly known instance of AI flying a fully operational fighter jet in combat conditions. Risk: Europe lags critically in AI chips (just 6% of global AI chip VC, 2022–2025), U.S. defence-tech investment still runs ~3x higher, and Ukraine’s rejection of Helsing HX-2 drones on performance grounds is a cautionary note on contested-environment readiness.

🇮🇳 🇰🇷 The Emerging Powers: India and South Korea Swing states of the Indo-Pacific autonomous arms race

India deployed its ARCV robotic mule on the China-India border in 2025 — the first autonomous ground vehicle in the LAC theatre — and is advancing a 50 kW directed-energy weapon following its April 2025 30 kW laser test. Its domestic drone investment is explicitly designed to challenge Chinese MALE dominance in South Asia. South Korea’s LIG Nex1 quadrupedal robots are among the most advanced military-grade ground robotics programmes outside the U.S.; the country is investing heavily in counter-UAS R&D driven by the North Korean drone threat and Taiwan contingency implications.

Sources: StartUs Insights, 2026; McKinsey, February 2026; Georgetown CSET, September 2025

Comparative Spending & Investment Snapshot (2025–2026)

| Country / Bloc | Defence Spending (2025) | Defence-Tech VC (2025) | Key Autonomous Programme |

| United States | ~$967B (3.38% GDP, 2024) | $14.2B equity | Drone Dominance / DAWG / Anduril Arsenal-1 |

| China | ~$220B official; est. $515B PPP | State-directed MCF | PLA Intelligentization / 15th Five-Year Plan |

| EU (combined) | €381B (+11% YoY, 2.1% GDP) | €2.6B (from €200M in 2021) | ReArm 2030 / Helsing / EDIP €1.5B |

| Turkey | Undisclosed (rising) | Domestic | Baykar TB3/Kizilelma; STM Kargu swarm |

| Israel | ~5.3% GDP (est.) | Domestic / US | Iron Beam 100kW; IAI Harop; Rafael |

| Ukraine | ~34% GDP (wartime) | $129M+ (2025) | Swarmer IPO; 200K drones/mo; 15,000 UGVs |

| India | ~$74B (2.4% GDP) | Growing | ARCV; 50kW DEW; domestic MALE programme |

| South Korea | ~$46B (2.7% GDP) | Growing | LIG Nex1 quadrupeds; counter-UAS R&D |

II. The Regulation Race: Governance Collapsing Behind Capability

The systems described in this series — Kargu swarms, Swarmer’s combat AI, the Orchestrator’s voice-commanded fleets — are fielded and operational. The treaties that were supposed to govern them do not exist. The UN General Assembly’s December 2024 resolution (166–3, Russia/North Korea/Belarus dissenting) endorsed a two-tier LAWS framework — monitoring for some systems, potential prohibition for others — but it is non-binding, its definitions unresolved. China considers only unstoppable systems autonomous; France incorporates any device capable of independently selecting targets. That gap reflects fundamental disagreements no treaty process has resolved in four years.

Multiple deployed systems already exploit the definitional void. Russia’s Marker selects targets semi-autonomously. Israel’s Harop homes autonomously on radar emissions. Turkey’s Kargu-2 lets one operator authorise 20 simultaneous lethal strikes. Ukraine’s Swarmer sequences strikes without per-engagement authorisation. All are technically compliant with their governments’ stated positions; all push against the conceptual foundations of international humanitarian law.

The EU’s emerging export control framework is the most consequential near-term regulatory development — not a treaty. If the EU mandates human-oversight architecture as a condition of defence exports, it creates a de facto two-tier global market: trusted-AI systems (EU/U.S.-compliant) versus unrestricted systems (Chinese, Turkish). Meanwhile, DoD Directive 3000.09’s ‘appropriate human judgment’ standard is eroding in practice: the Orchestrator Challenge explicitly requires fleet-level plain-language commands, not individual engagement authorisations. That is a policy shift embedded in a procurement specification — not announced in a press release.

Sources: UN GA Resolution A/79/88, December 2024; TRENDS Research & Advisory, 2025; EU Readiness 2030; FY2026 NDAA Section 737

III. Investment & Funding: The Capital Architecture of Autonomous Warfare

The $49.1 billion in defence-tech VC recorded in 2025 is the capital architecture of a new military-industrial order being built in real time. American startups captured $14.2 billion — nearly three times European peers. The top three rounds alone (Anduril $2.5B Series G, Saronic $600M Series C, Helsing €600M Series D) raised more than the entire global defence-tech sector did in 2020. PitchBook predicts that a legacy prime will acquire a venture-backed defence-tech startup at scale in 2026 — the clearest signal yet that the new military-industrial order is not disrupting the old one, it is absorbing it.

The structural headwind is supply chain. The small drone ecosystem remains predominantly dependent on Chinese components — flight controllers, motors, FPV cameras. The FCC’s January 2025 implementation of NDAA Section 1709 crystallised the problem without solving it: Red Cat’s stock rose 60% on the enforcement news, but its $38–41M in FY2025 revenue is a rounding error against China’s 60–70% control of global small-drone component supply. Tariff volatility (BlackRock Geopolitical Risk Dashboard, 2026) compounds the exposure for any COTS-dependent U.S. manufacturer. Battery density — the binding constraint on long-endurance maritime and HALE platforms — is similarly concentrated in the same Chinese supply chain the Covered List is designed to restrict.

Sources: PitchBook / Defense News, January 2026; CB Insights, 2025; Crunchbase, November 2025; McKinsey European Defence Dashboard, February 2026

Top Defence-Tech Funding Rounds 2025 (Selected)

| Company | Country | Round | Amount | Valuation | Domain |

| Anduril Industries | USA | Series G | $2.5B | $30.5B | Multi-domain autonomy |

| Helsing | Germany/UK | Series D | €600M (~$692M) | €12B (~$14B) | AI defence / drones |

| Saronic | USA | Series C | $600M | $4B | Autonomous USVs |

| Shield AI | USA | Various | $1.3B total | $5.3B | AI pilot / CCA |

| Swarmer | Ukraine/USA | Series A | $15M | Filing Nasdaq IPO | Combat swarm AI |

| Chaos Industries | USA | Series C | $275M | $1.1B | AI threat detection |

IV. Synthesis: Four Conclusions for the Decade Ahead

1. The Factory Gap Is the Decisive Variable

The decisive variable in the 2026–2035 competition is not algorithmic sophistication — it is factory throughput. China targets one million tactical UAS by 2026; Ukraine produces 200,000 FPV drones per month; Arsenal-1 targets tens of thousands of autonomous systems annually. The U.S. produces the most capable individual systems. China produces the most systems. Turkey and Ukraine produce the most cost-effective at scale. None of these is the same country. Neither the Orchestrator Challenge nor Arsenal-1 closes the unit-cost and production-volume gap with China’s civilian-industrial complex on a ten-year horizon without structural procurement reform that goes beyond any single programme.

2. The Regulatory Gap Will Not Close Before It Matters

The Kargu-2 live-fire test, Swarmer’s 70,000+ AI-coordinated combat missions, and the Orchestrator’s fleet-level plain-language command architecture have each crossed thresholds that UN working groups are still debating in abstract. The regulatory gap is not narrowing — it is widening at the pace of the technology. The most consequential near-term development is not a treaty (which will not exist within this decade under any plausible scenario) but the EU’s export control framework, which may create a durable de facto two-tier global market.

3. The Investment Flywheel Is Self-Sustaining

At $49.1 billion in 2025 — nearly one in eight VC dollars globally — defence-tech investment has crossed the self-sustaining threshold. Valuations place software-first companies (Anduril $30.5B, Helsing €12B) alongside legacy primes. The predicted 2026 acquisition of a venture-backed defence-tech startup by a legacy prime will signal the new military-industrial order is not disrupting the old one — it is absorbing it.

4. Ukraine’s Data Is the Most Valuable Strategic Asset

No military, research programme, or test range has access to the combat data Ukraine has generated since February 2022: four years of high-intensity peer conflict across autonomous systems performance, jamming responses, swarm coordination, UGV logistics, and directed-energy countermeasures. That dataset — held in Swarmer’s algorithms, 270+ UGV manufacturers’ design choices, and millions of drone missions — is a first-order strategic asset. Ukraine’s post-war integration into NATO’s defence-industrial base is not merely a political question about alliance membership. It is a technology strategy question about who gets to learn from the world’s most consequential autonomous weapons laboratory.

Sources: PitchBook / Defense News, January 2026; McKinsey, February 2026; EU Council Readiness 2030

The autonomous weapons decade will not be won by the country with the most sophisticated drone or the best AI model. It will be won by whoever solves the integration problem — converting capital, combat data, manufacturing throughput, and governance legitimacy into fielded, trusted, scalable capability before their adversaries do. The series closes on two factory floors: Arsenal-1 in Ohio and a UGV assembler’s garage in Zaporizhzhia. Both are making the same bet — that the future of warfare is built by whoever ships fastest. One has $30 billion in venture capital. The other has a three-year runway before the war either ends or escalates beyond what any factory can absorb. |

Key Sources & Expert References

Defense News: ‘Defense-Tech Startups Had Their Best Funding Year Ever in 2025,’ January 2026 — defensenews.com

PitchBook: Defence-tech VC data 2024–2025 — pitchbook.com

McKinsey: European Defence Dashboard, February 2026 — mckinsey.com

EU Council / European Defence Agency: EU Defence in Numbers 2025 — consilium.europa.eu

NATO: Hague Summit Declaration, June 2025 — nato.int

Georgetown CSET: ‘Pulling Back the Curtain on China’s Military-Civil Fusion,’ September 2025 — cset.georgetown.edu

Foreign Affairs: China PLA civilian tech adoption, October 2025 — foreignaffairs.com

Helsing: Series D Announcement, June 2025; CA-1 Europa reveal, September 2025 — helsing.ai

TRENDS Research & Advisory: ‘The Backlash Against Military AI,’ 2025 — trendsresearch.org

UN General Assembly: Resolution A/79/88, December 2024 — un.org

BusinessWire: Swarmer $15M Series A, September 2025 — businesswire.com

StartUs Insights: Defence Industry Report 2026 — startus-insights.com

{kind=link}

Leave a comment