As humanoid robots move from prototypes to production, the divide between China’s hardware-driven ecosystem and America’s AI-first ambition has never been sharper. The contrast tells a story not only of divergent innovation models, but of two nations betting on different visions of the future of embodied intelligence.

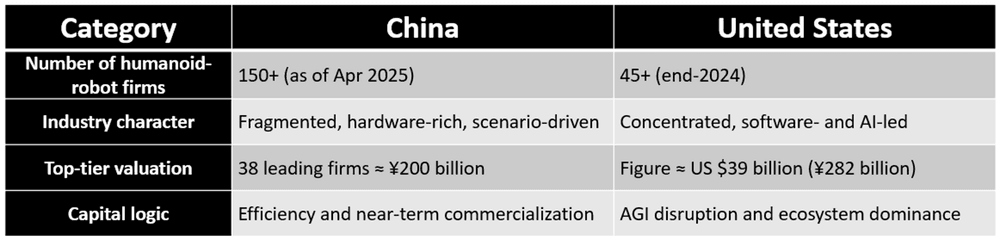

China’s frontrunners—UBTech (valued > ¥60 billion), Unitree, and Zhiyuan Robotics (¥15 billion)—collectively exceed ¥200 billion in valuation. Yet that still trails one company: Figure, whose US $39 billion valuation outstrips the combined total of China’s major players.

The Diverging Roads to the Future: How China and the U.S. Are Building Their Humanoid Dreams

In the global race toward humanoid intelligence, China and the United States are taking profoundly different routes—each shaped by its own industrial DNA, capital logic, and national ambition. While Chinese companies are forging ahead through the brute force of manufacturing and supply-chain mastery, American players are betting everything on the promise of software-defined intelligence and the long-term realization of artificial general intelligence (AGI). The result is not merely a technological rivalry, but a clash between two civilizational approaches to innovation—one grounded in scale and pragmatism, the other in vision and abstraction.

China’s Hardware Confidence

To understand China’s momentum in humanoid robotics, one must start with its unmatched hardware ecosystem. The Pearl River Delta, stretching across Shenzhen, Dongguan, and Guangzhou, has evolved into the world’s most efficient engine for building intelligent machines. Motors, servo drives, sensors, harmonic reducers, and structural components can all be sourced within a two-hour radius. For startups, this means prototype cycles that last days instead of months and costs that undercut Western counterparts by a factor of three or more. Such industrial efficiency has lowered entry barriers, fueling the rise of more than 150 humanoid-robot ventures across the country by mid-2025.

Beyond infrastructure, China’s demographic and economic landscape provides fertile ground for automation. With an aging population and labor costs climbing year by year, “machine-for-man” has become more than a slogan—it is a national necessity. Robots are no longer confined to futuristic research labs; they are appearing on automobile assembly lines, in appliance factories, logistics centers, and even shopping malls. This abundance of real-world use cases gives Chinese companies an unparalleled testing field for technical validation and iterative improvement.

Meanwhile, capital and policy are moving in lockstep. In the first quarter of 2025 alone, over 30 humanoid-robot investment rounds were recorded in China, a signal of both investor confidence and government prioritization. From the national “Future Industries” roadmap to provincial subsidies in robotics clusters, the alignment between the state, capital, and industry has created a self-reinforcing cycle of innovation. In short, China’s humanoid boom is powered by the trinity of supply-chain speed, market hunger, and political intent.

America’s Software Ambition

Across the Pacific, the United States has chosen a different battlefield—one defined less by production volume and more by cognitive aspiration. Silicon Valley’s worldview has always been “software eats the world,” and in the humanoid era, that ethos translates to “intelligence defines the body.”

No company captures this vision more clearly than Figure, the California-based startup that has become the face of the American humanoid dream. Rather than focusing on individual task performance, Figure is building Helix—a large-scale, end-to-end “vision-language-action” model designed to give robots general reasoning and adaptability. In the words of one investor, Figure is not just building a robot—it’s “training a mind.”

Such ambition comes with extraordinary capital backing. In its Series C round, Figure secured over US$1 billion, led by Nvidia and Intel Capital. The funding will expand production capacity, build out GPU compute infrastructure, and fuel massive data collection to strengthen Helix’s learning pipeline. These are not investments in metal or motors; they are bets on neurons and networks—the robot’s brain and nervous system rather than its limbs.

Moreover, Figure’s long-term strategy reaches beyond manufacturing. Like Google with Android or Microsoft with Windows, it aims to become the operating system of robotics—a platform that others license, build upon, and depend on. Such a role would position Figure at the core of a future robotic ecosystem, collecting data and influence across industries. The result is a valuation of nearly US$39 billion, a figure that dwarfs the combined worth of China’s top 30 humanoid startups.

Diverging Valuation Logics

The valuation gap between China’s humanoid firms and America’s Figure reveals two distinct philosophies of value creation—what might be called the pragmatist’s present value versus the dreamer’s option value.

Chinese companies are grounded in near-term results: unit economics, component costs, production efficiency, and customer contracts. Their valuations reflect tangible capability—robots already deployed on factory floors, reducing labor costs or improving quality control. It is a logic of precision manufacturing and incremental innovation.

By contrast, Figure’s valuation represents a financial option on the future. Investors are not buying today’s revenue—they are buying the possibility that Helix becomes the first true AGI-enabled robot platform, capable of reasoning, learning, and interacting across industries. The $39 billion figure is not a reflection of today’s balance sheet; it is the market’s collective wager on who might define tomorrow’s intelligence standard.

Shared Challenges, Different Crossroads

Both ecosystems face serious headwinds. China’s risk lies in hardware over-competition—too many companies chasing incremental gains, driving prices down while struggling to differentiate on core AI capabilities. Without breakthroughs in algorithms, perception, and reasoning, the country’s humanoid revolution could plateau below the intelligence threshold required for global leadership.

The United States, on the other hand, faces the opposite challenge: a chasm between dream and delivery. End-to-end AI frameworks like Helix remain largely unproven in the real world, and scaling them to stable, affordable systems will require enormous computational and financial resources. A single misstep in technical feasibility—or a delay in commercialization—could quickly deflate Figure’s lofty valuation.

Convergence—or Collision—Ahead

Yet the story is far from zero-sum. As both nations advance, their trajectories are likely to converge in unexpected ways. Chinese companies are already pouring resources into AI model development, while American firms will inevitably need to address the realities of manufacturing scale and cost. This opens the door to a new global division of labor: America could design the “brains” while China builds the “bodies.”

Ultimately, the decisive factor will not be who dreams bigger, but who delivers first. The true winners of the humanoid race will be those who can deploy robots profitably and at scale—on factory floors, in logistics centers, in homes, and beyond. Grand visions and national strategies aside, it is practical adoption that will define the next phase of the humanoid revolution.

As one analyst put it succinctly: “The future of humanoids won’t be won by who codes the smartest brain or builds the strongest muscle—but by who first teaches them to work, reliably, in the real world.”

{kind=link}

Leave a comment